2013 Mid-Year Municipal Market Update

The bond market experienced sharp, rapid adjustment in the second quarter — arguably the greatest since the fall of 2008. The 10-year Treasury bond yielded 1.63% in early May and finished June yielding 2.49%. As of June 28, year-to-date it had lost 2.57% of its value.

The 10-year, “AAA” rated Municipal Market Data (MMD) municipal bond index reacted similarly during this two-month period ending June with a yield of 2.56% compared to 1.90% as of May 28. The recent rise in bond yields translate into significant price declines sparing few, if any, bond investors. For some, forced to sell during the tumult, it was a bloodbath reminiscent of Q4 2008 and Q1 2009.

The Great Rotation debate

Certain pundits claim the increasing bond yields of the last few months mark the beginning of the “Great Rotation” from bonds into equities and record amounts of cash coming off the sidelines. No one can be certain at this point if the cycle has turned. It is too early to tell in our view as we keep in mind several times post Q3 2008 when Treasury bond yields increased by 50-60 basis points only to subsequently see bond prices rally and yields fall. Certainly we are wary bond investors, but we have seen this before.

A case can be made perhaps that the recent bond sell-off presents a short-term, attractive buying opportunity. Some of the best investments we made for our clients in recent years occurred when we invested client cash in the last quarter of 2008, the first quarter of 2009 and in 2010 following the airing of the well-known “60 Minutes” municipal bond market segment. If the Fed does not sell in quantity, prices will stop falling and may reverse their recent trend.

Separate account, laddered portfolios vs. municipal bond funds

Almost universally, our client’s separate account, laddered portfolios handled last quarter’s turmoil much better than the broader bond market. This is a similar storyline to what our clients’ portfolios experienced during the 2008-2009 financial crises. These portfolios avoided much of the damage resulting from the panicked selling of many bond funds, bond ETFs and hedge funds. In contrast, the June experience of many bond fund and ETF investors was bad. Fund investors unloaded shares at a record pace — $6 billion worth in two weeks — forcing some funds to sell bond holdings to dealers at a time when prices were plummeting. These funds recorded significant losses.

One thing we know with certainty after three decades specializing in this business: it is difficult to hedge or effectively short the municipal market and when municipal bond funds are forced en masse to sell bonds to meet redemptions, losses for shareholders are magnified. For example, the iShares S&P National AMT- Free Muni Bond (MUB) lost 1.76% in value in ONE week (June 13-20) and the Pimco Total Return Fund lost 2.59% in June. Certain “inflation protected” funds lost more than 6% of their value in the second quarter. Many investors learned in June share sale prices can veer significantly from NAV in a market rout because the funds’ advertised liquidity feature tends to disappear.

Here is an excerpt from our November 2008 market update

“This financial crisis has reinforced in our minds the significant advantage enjoyed by investors who use a SEPARATELY MANAGED, NON LEVERAGED bond portfolio strategy. This approach to bond investing lessens your volatility and increases your liquidity……..Among other things, separate account management allows for quality investments to be held when the market moves sharply downward. There are no forced sales in a separately managed bond portfolio unlike what often occurs in bond funds when prices plummet. When the general market recovers, so does the paper value of your investment………Additionally, if you need to raise capital you simply request bids for a portion of the bond portfolio; even in this market, you will find bidders for smaller blocks of quality, shorter maturity, fixed rate bond issues. This simple strategy has worked well for decades and we expect that won’t change anytime soon.”

We are not downplaying the reality that separate account portfolios lost value over the past two months. We remind you investing in the bond market entails risk, which can result in losses.

Importantly, recently incurred portfolio paper losses for the most part will be offset over time as income and maturity proceeds are reinvested into higher yielding bonds. For income-oriented investors, adhering to a disciplined strategy of investing in quality bonds laddered over an intermediate time frame remains the soundest way to invest in the municipal bond market.

Separate account, laddered portfolios vs. money markets

We have had many conversations recently with concerned clients about the recent decline in portfolio valuations. Some fear what will happen if interest rates continue to rise and bond prices decline further. Some have asked, “Would I be better off selling my bonds and just holding cash until bond prices stop falling?” After all, as yields increase, the yield on cash should grow in tandem, while existing bond prices would decline in value as yields rise. This would lead one to reasonably wonder if a simple money market fund investment would outperform a fixed maturity, laddered bond portfolio. One of our portfolio managers, Scott Rausch, CFA, recently prepared a couple of scenario analyses that look at this very issue.

The first is a simplified scenario consisting of a $1.2 million, equally laddered municipal bond portfolio spread over six years (i.e. $200,000 par maturing in each year). Bond quality is split 40% to 60% between “AAA” and “A” rated bonds, respectively, and initial yields are based off of actual Municipal Market Data (MMD) levels for bonds settling August 1st of this year. This portfolio is compared to a tax-exempt money market fund, which currently yields zero percent.

These portfolios were then exposed to a 100 basis point increase in interest rates, applied to all maturity dates, at the end of each twelve-month period. Maturing bonds and income from the bond portfolio were rolled over at the new, higher six-year rate each year. Even in this extreme rising rate environment, the bond portfolio only trails the performance of the money market fund by 26 basis points on an annualized basis (2.23% for the bonds versus 2.49% for all cash). However, tax-exempt income for the bond portfolio is greater — $217,248 versus the money market’s income of $190,473. The laddered portfolio delivers higher income.

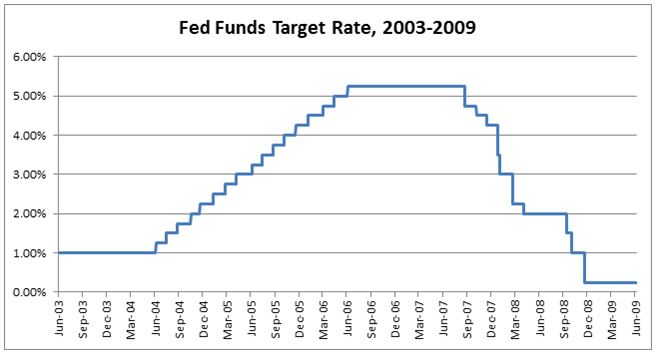

This is an interesting exercise in bond math, but a six-year run of yearly 100 basis point rate increases across the entire yield curve is unlikely to actually occur. Thus, we looked at recent history for a more realistic scenario, and focused on the period from June 2003 to June 2009.

The burst Internet stock bubble fed into a recession that started in March 2001, and was exacerbated by the economic shock resulting from the September 11th attacks. In reaction, the Federal Reserve embarked on a series of cuts in the Federal funds rate, reaching a then unheard-of 1.00% in June 2003. As the economy improved, the Fed gradually raised short-term interest rates over a two-year period from 2004 to 2006. This rate then stabilized for 15 months, and dropped precipitously over the next 15 months.

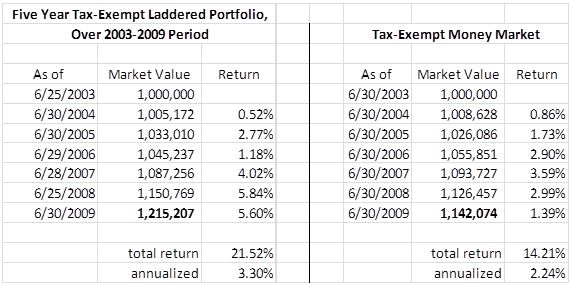

We used municipal bond yield data from this period to create a $1 million tax-exempt portfolio. The model portfolio has $200,000 par value maturing each June over a five-year ladder. Our kickoff date is June 2003, when the Fed funds rate bottomed out. Each June, maturing bonds and all income are reinvested at the new five-year bond yield. The model assumes a 40% to 60% weighting of “AAA” rated and “A-“ rated general obligation bonds, respectively. Spot bond yields for our 2003 kickoff and each succeeding year are based directly on the Bloomberg fair market curve indexes for the relevant maturity dates. The results of the tax-exempt money market fund are based on actual returns of the Vanguard Tax-Exempt Money Market Fund during this period. Here are the results:

As you can see, the laddered bond portfolio lags behind the money market fund in two of the first three years, but as each tranche of the bond portfolio matures, the proceeds and all interest are reinvested at the new five-year yield. In all years over the actual five-year reinvestment period, the $200,000 par value maturity proceeds are reinvested at higher rates than that tranche’s original yield.

As an example, three years into this model as June 2006 arrives, the $200,000 that had been producing cash flow at a 1.66% yield is reinvested in June 2011 bonds yielding 4.10%. This is a 244 basis point increase. As you can see, as time progresses the laddered portfolio outperforms, as more and more of its assets are locked into higher yielding bonds.

The outperformance of the laddered bond portfolio, in part, reflects the power of compounding interest from higher yielding bonds found at different points of the historically upward-sloping yield curve. This dynamic helps to cushion the lesser paper value of some bonds held at lower yields. Additionally, any unrealized paper losses on lower yielding securities diminish as maturity approaches, becoming zero at payoff.

The average U.S. economic expansion lasts three and one quarter years, per the National Bureau of Economic Research. Eventually, interest rates and bond yields decline, as they have always done. When this begins to occur, the higher yields captured in the laddered portfolio will significantly outperform cash.

Finally, the tax-exempt income for the bond portfolio is $177,377 — versus the money market’s income of $142,074. The laddered portfolio delivers higher income and higher total return.

Opportunistic investing in imperfect markets

This brings us to a critical point — our model does not take into account any sort of competent, active management. It makes no allowance for opportunistically capitalizing on market mispricings, or for superior credit analysis, or for any other value-added feature of our bond portfolio research and management process. The municipal bond market is, by its vast and disparate nature, inherently less efficient than the U.S. Treasury or high-grade corporate markets. Our clients’ portfolios benefit from this dynamic.

Our analysis also excludes the issue of tax loss harvesting swaps by which the bond manager takes losses in carefully selected, lower coupon bonds so that the client can shield income from another source. Sales proceeds can then be invested at new, higher-yielding tax-exempt securities. This can benefit investors seeking maximum tax efficiency and the further enhancement of portfolio returns.

For income oriented investors with a mid- or long-term perspective, we see a notable benefit to rapidly rising yields and an imperfect market — the opportunity to take advantage of heavy selling by bond fund and ETF managers who are forced to sell bonds to meet the redemptions of panicked investors. We have seen this many times over several decades managing bond portfolios. We recently saw this in June, as multiple investors tried to sell similar bond holdings at the same time, with sellers greatly outnumbering buyers, leading to a significant decline in prices.

When these markets occur, we try to avoid selling and try mightily to add quality credits at attractive yields to client portfolios. We did this two months ago. We did this in 2010. We did this in 2008-2009. And we will do it again in the years ahead.

Periods when bond prices drop significantly and yields increase in a short period of time present wonderful investment opportunities for a committed fixed income investor.

This is not the end

The market events of the past few months give us a glimpse into our bond market future. It has been quite a stretch, no doubt, and we expect more future volatility.

Today, market liquidity is more tenuous than in past years. This is the result of dealers holding less inventory, increasing regulatory requirements, a smaller investor base and more retail ownership through mutual funds and ETFs rather than direct holdings. This liquidity dynamic may cause problems and anxiety for ephemeral bond investors. For committed investors with separate account management, laddered portfolios this dynamic are less problematical. In fact, a market like we are currently experiencing can offer wonderful investment opportunities.

A silver lining in June’s storm cloud: when a bond investor is selling at distressed prices there usually is another investor buying. Expect more price volatility and remember that volatility often brings opportunity.

The current state of the bond market reminds me of Sir Winston Churchill’s observation in November of 1942, “Now this is not the end. It is not even the beginning of the end. But it is, perhaps, the end of the beginning.”

Opportunity in muniland — remembering, why bonds?

We believe last quarter’s disorderly secondary market with its diminished level of liquidity portends one bit of good news for income oriented bond investors: higher nominal and relative yields and therefore better incomes.

In our view here are the reasons for investing in bonds: income, safety, and the stability of principal over an intermediate time period. Despite the sell-off of recent weeks, quality municipal bonds still hold the characteristics that make them alluring to investors. They offer a cushion against stock market volatility, security of principal and a steady income stream exempt from federal income taxes.

Clearly, today’s market requires a high degree of credit discrimination. We have long stated that “municipal bonds are not all created equal” and focused our credit research expertise on the “three pillars”: underlying credit quality, deal purpose and deal structure. This credit discipline is critical in today’s market.

The municipal bond market is arcane and idiosyncratic and that is not going to change anytime soon. This dynamic provides excellent investment opportunities for the committed, income oriented investor. Generally speaking, today’s current market offers excellent value.

Examine Bernardi Securities, Inc. composite portfolios’ 12 year performance numbers and you see consistent, increasing value over many different market cycles. As disquieting as it is to see a 6/30/2013 portfolio valuation down from its earlier year value, the paper losses will be partially offset in the coming months by greater monthly cash flows as reinvestment occurs. Over time this changing dynamic is a positive for income oriented bond portfolios. If you are not convinced, review the value of your bond portfolio as of 10/31/2008 and then again its value 7 to 9 months later. Additionally, some of the best performing bonds in your portfolio today are those bought in late 2008 and early 2009 when bond prices declined significantly.

The bond market sell-off last quarter reminded us again — a separate account, quality, laddered bond portfolio strategy works very well for income-oriented investors who do not have a short-term perspective.

Thank you for your continued confidence in our bond portfolio research and management process. Please call us if you would like to review the portfolio or if you have any questions.

Sincerely,

Ronald P. Bernardi

President and CEO

August 14, 2013