Market Anxiety From One D-Word to Another

-

Moody’s “Corporate Default Rate to Breach Historical Levels”

-

Three of four of the largest U.S. bank failures have occurred in the past two months

-

Capital One: “Credit Card Delinquencies Test Multi-Year Highs as Job Market Faces ‘Material’ Worsening.

-

Powell: Monetary Policy Trying to Reach and Stay at Sufficiently Restrictive Stance to Bring Inflation Down –WSJ

The headlines above demonstrate that investors need greater focus on the credit health of their fixed income investments in this phase of the economic cycle.

Because inflation remains above the Fed’s 2% target, monetary policy will remain restrictive for longer, placing further pressure on the economy.[1] Investors’ concern about duration risk (maturity length) should pivot to the increasing threat of credit and default risk. Warren Buffett famously quipped “Only when the tide goes out do you learn who has been swimming naked.” The Fed has been the force causing the tide to ebb and by draining liquidity from the system, its actions are further generating pressure on the economy.

At this point, acute pressure within the economy has been sector and company specific. For example, certain banks have fallen victim to interest rate risk within their fixed income portfolios and clearly failed to properly manage this risk. Today’s much higher rates (compared to 1-3 years ago) caused paper losses within bank fixed income portfolios. Many banks can avoid realizing these losses because their deposit base is stable.

However, due to a concentrated deposit base and then substantial depositor flight, Silicon Valley Bank, Signature Bank, and, most recently, First Republic failed. These failures are primarily a reflection of a rate shock rather than a credit shock. These recent failures compel us to ask two questions: could this be the next phase of the economic cycle and is the market underappreciating this possibility?

Interest Rate Risk Within Municipal Portfolios:

Interest rate risk is mitigated in part by the ladder structure – as there will always be coupon interest and short term maturities coming due for reinvestment or to meet unforeseen cash needs. Furthermore, high coupons[2] are a way to lower duration and protect against inflation risk by boosting portfolio cash flow. That said, we believe the market is generally overpaying (low yield offered) for coupons 5% and above. We believe 3.50-4.50% coupons offer a sweet spot of high cash flow and an attractive yield.

Currently, the market is inadequately focused on credit risk as demonstrated by:

- Corporate credit default swap levels – These are a measure of credit risk within corporate bonds. The higher the spread, the more credit risk the market attributes to buying a corporate bond. These spreads are below 2022 and 2018 highs. The latter was the last time there was a significant probability of a recession pre-COVID.

- 10-year municipal ratio – The 10-year municipal yield divided by the 10-year treasury yield is below historical averages. This ratio typically moves higher and above historical averages during times of market stress and concern over credit fundamentals within the municipal universe.

The muni market’s quiescence is somewhat understandable, given state cash reserves are at record levels. This provides a massive buffer to weather a downturn. But should growth slow or remain muted for an extended period, the large levels of reserves will deteriorate. As an example, the State of California’s projected deficit has increased by over $10 billion since January alone, now projected to be $32 billion in total. At this point, the state will primarily cut expenses in order to bridge the gap and only pull $450 million from reserves.

This demonstrates the immense budget flexibility states have in order to address shortfalls. It is also a reason the municipal credit cycle tends to lag the general economy as municipalities can “kick the can” for an extended period. Even though the Great Financial Crisis was the hair that broke Detroit’s fiscal back, the city did not file for bankruptcy until 2013.

Corporate issuer credit health is more sensitive and tighter correlated to the economy versus your average municipal obligor. Moody’s Investors Service recently noted it expects US corporate default rates to climb. Moody’s projects the US speculative-grade default rate rising to 5.6% a year from now, breaching the historical long-term average of 4.7%. It cited lower rated issuers coming under pressure from higher interest rates, slower economic growth, and limited market liquidity.

Some municipalities are dealing with budget shortfalls and lack substantial rainy day funds to help cushion forthcoming cutbacks. Many entities relied heavily on Federal largesse through the American Rescue Plan Act (ARPA) to bridge their finances, and now will likely need to organically address deficits and structural imbalance. For example, New York City is expecting a potential $4 billion deficit this year. And the State of Illinois recently revised down its revenue projection from $51.4 billion to $50.7 billion.

According to a recent Route Fifty article[3]:

Almost all the states with income taxes that have reported April receipts—including Alabama, Arkansas, Idaho, Iowa, Kansas, Missouri and Montana—have seen revenue declines. West Virginia is the only exception, reporting a 4% year over year increase in total April general fund revenues.

This apparent path forward to tighter budgets and reduced Federal support, means portfolios should avoid:

- Fiscally imbalanced issuers with large, fixed costs (pensions, OPEB, debt service)

- Fiscally unprepared issuers with low unrestricted cash balances

- Bond issues with high levels of sensitivity or concentration to economic growth.

- Urban environments (with the fiscal characteristics of item i. or ii. immediately above), which are suffering from lower foot traffic, higher crime, and deteriorating commercial real estate values.

Our portfolio management strategy continues to target essential purpose and essential revenue bond issues from small-to-medium size issuers that have either fiscal flexibility and/or lower fixed costs. In many of these cases, these types of issuers do not face the same type of secular pressure that working-from home, deteriorating commercial property prices, and crime are causing for many larger, urban creditors.

Hiking in May, Cutting in July

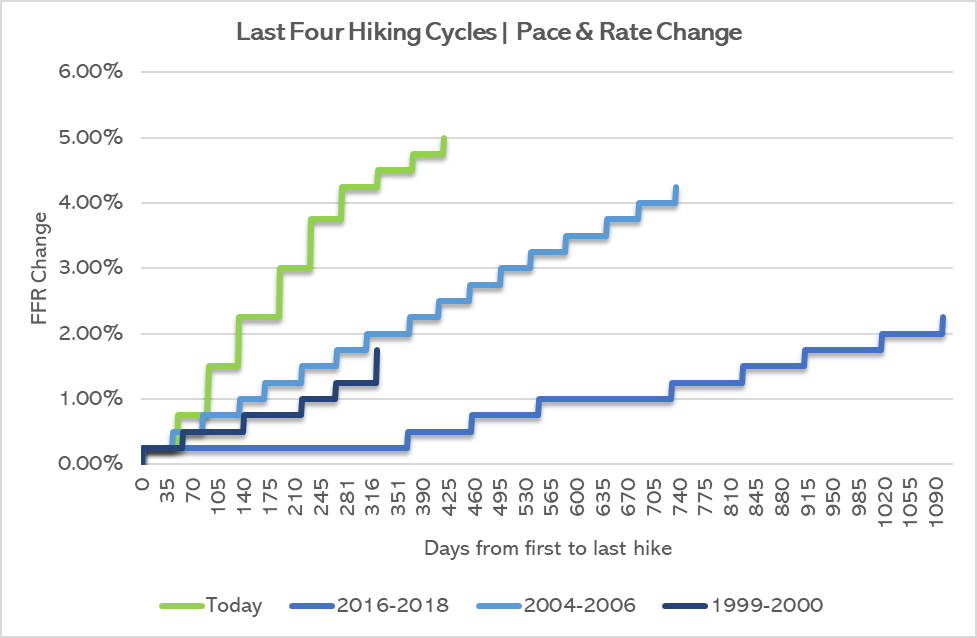

The rate hike cycle has been exceptionally severe in both pace of change and change itself (5% increase in rates in just over 400 days). The Fed recently hiked to 5.25% on May 3rd. And the market’s current lack of concern over credit conditions is primarily predicated on a Fed “pivot” to lower rates and easier monetary policy in the near future.

The market is anticipating a 33% chance of a rate cut (from 5.25% to 5.00%) during the Fed’s July 26th meeting. The view is that a deteriorating economy and inflation will cause an abrupt change in Fed policy from hiking in May to cutting in July, and beyond.

The impact of rate hikes is known to have a lagging impact on the economy. The Fed acknowledged this in their recent FOMC statement:

the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation…

Their recent decision to “pause” rate hikes is based on them wanting to surveil the lagging impact of their policies and that it likely will slow inflation from today’s still high levels.

Yield Curve & Where We See Value

The municipal yield curve has been fluctuating between a J and nearly U shape given high short term rates (induced by the Fed) and upward sloping longer terms yields. The positively sloped municipal curve is unlike the inverted treasury yield curve where shorter maturities generally yield more than longer ones:

| Treasury Tenor | Yield |

| 3-month | 5.18% |

| 1-year | 4.77% |

| 2-year | 4.00% |

| 3-year | 3.67% |

| 5-year | 3.46% |

| 10-year | 3.49% |

| 30-year | 3.83% |

Ultra Short Strategies: At the very front end of the yield curve, we find bank certificates of deposit (~5%), treasury bills (~5%), and tax-exempt municipals (~3%) attractive.

Tax-exempt money market funds have been a great cash placeholder and have fluctuated in yield anywhere from 2.50-4.00%(tax-exempt) over the past month. These are floating rate funds composed of variable rate obligations backed by investment grade municipal issuers with average maturities measured in days.

Tactical Ladder: the benchmark municipal yield curve in 2-10 year maturities is quite rich (low yield/ratios) in our opinion. Unless we can capture a 3% yield to worst, we tend to favor parking funds in the money market fund and opportunistically invest. 10-20-year bonds yield 3.50-4.00% are very attractive in our opinion.

A 4.00% tax-exempt yield is equivalent to 6.34% taxable. We deem this not only a great return to lock-in within the municipal universe, but relatively attractive to many other asset classes as well.

In Summary

Given the reality of inflation above its 2% target, the Fed is likely committed to a tight monetary policy for longer inducing further economic weakness. Given this scenario we believe the market is overestimating duration risk to portfolios and underestimating the credit risk and the health of their fixed income holdings. Therefore, it is time to allocate to high-grade credits.

Resulting higher municipal ratios – during a period of lower or muted growth – will be welcomed. This is traditionally a great buying opportunity for investors.

Thank you for your confidence in our team and please reach out to your Investment Specialist or Portfolio Manager with any questions you may have.

Sincerely,

Matt Bernardi

Vice President

May 2023

[1] The last consumer price index (CPI) report was released on May 10th and printed at 4.9% year-over-year.

[2] A bond’s coupon is the annual cash flow you receive based on the par amount purchased. A bond’s yield, however, takes into account the price you pay and is the true return on the bond if held to maturity/call. A 4% coupon bond purchased at par ($100) has a 4% yield. A 4% coupon bond purchased above/below par has a lower/higher yield than the coupon given the premium/discount paid and returned value on maturity ($100).

[3] https://www.route-fifty.com/finance/2023/05/amid-economic-uncertainty-april-state-tax-revenues-decline/386307/