Perspective for Advisors: Opportunity in Taxable Municipal Bonds

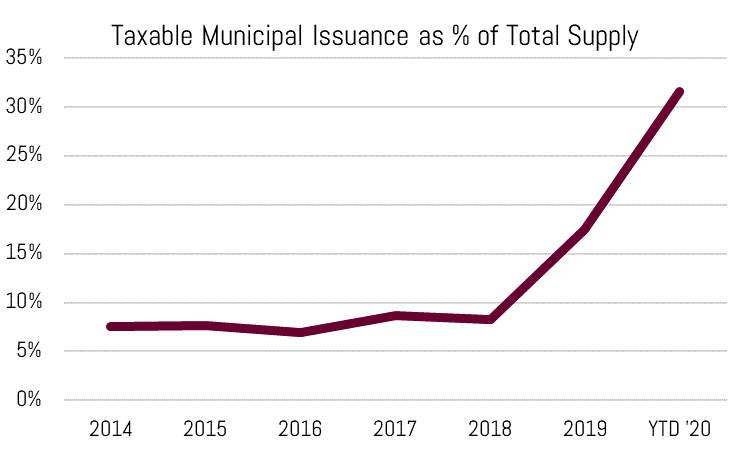

Taxable municipal bonds (taxable at the federal – and oftentimes state – income level) have historically lacked investors’ attention due to limited supply and presence in a market dominated by investors seeking non-taxable income. Supply has skyrocketed in recent years due to aspects of the 2017 tax reform bill, low nominal interest rates and a flat yield curve. Therefore, taxable municipals are more readily available, and they also offer attractive relative and risk-adjusted returns compared to other high-grade fixed income.

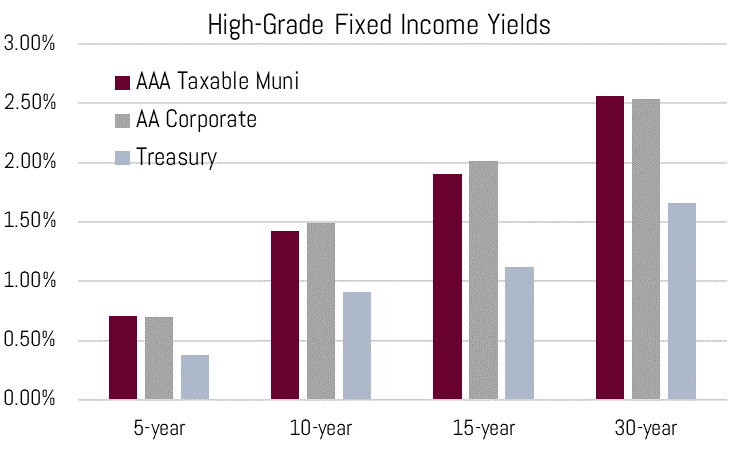

Source: SIFMA U.S. Municipal Bond Issuance Source: Bloomberg December 8th, 2020

As demonstrated above by the chart on the right, AAA rated taxable municipals (Bloomberg benchmark index) yield the same or more than the AA rated corporates (Bloomberg benchmark index), even though historical default rates are significantly lower. Equal or higher municipal yields are a result of a lack of direct Fed intervention in the municipal market, illiquidity premium, and general idiosyncrasies of the municipal market (e.g. many more CUSIPs/issuers relative to corporates). We think this dynamic is worth taking advantage of for retirement portfolios (i.e. IRA accounts) and certain investors with a federal income tax bracket below 30%.

2021 is poised to break this year’s record of taxable municipal issuance, but there are threats to future supply. For one, the bulk of the recent issuance is used for refinancing purposes due to the low rate environment. Should rates increase the ability to refinance will become more difficult likely reducing the new issue taxable supply. Additionally, if aspects of the 2017 tax reform are revoked, the supply of taxable municipals may decrease.

High-grade fixed income portfolio construction

Investor portfolios need to take a dynamic approach when considering taxable fixed income options. In most cases, taxable municipal bonds present the most attractive opportunity across the yield curve from a risk-adjusted or outright yield standpoint. However, corporates, U.S. agency securities, certificates of deposit, or treasuries may be more attractive in certain areas of the yield curve depending on market dynamics.

Based on today’s market dynamics taxable municipal bonds are an attractive opportunity for many investors.

Please contact your Investment Specialist for information about our Taxable Municipal Bond SMA strategies.