Update: COVID-19 and its Impact on Municipal Credit (Part III)

September 28, 2020

In Part III of our municipal credit commentary pertaining to the health and economic crisis brought on by COVID-19 we overview the most recent data available pertaining to state revenue surveys and data from municipalities within the State of Illinois. Thus far, the data indicates that some of the most dire revenue projections resulting from the pandemic lockdowns have not come to fruition as the resumption of economic activity has been stronger than expected.

That said, the impact of the pandemic has been broadly negative. We remain cautious on the outlook for the sector and as a result are targeting high quality, essential purpose, general obligation or essential revenue issues. We believe there remains downside risk in the most vulnerable sectors and the yield compensation for this additional risk is insufficient.

****

The full extent of revenue shortfalls at the state and local level as a result of the ongoing economic and health crisis will not be known for some time and will surely pressure both revenues and expenditures for years to come. In the early innings of the crisis some projections for the hit to state revenues were dire. The Center on Budget and Policy Priorities, for example, estimated revenue declines of up to 31% compared to pre-COVID projections.[1] The Federal Reserve Bank of Boston noted in July that the tax revenue for certain states could decline greater than 20% to 30%.[2]

However, recent J.P. Morgan analysis significantly contradicts the aforementioned “sky is falling” headline-grabbing projections. They found that that overall YTD tax revenue collections through July have been strong, and most states are only witnessing modest revenue declines of ~4-5%.[3]

Though revenue declines were significant during the depths of the social shut-ins, the recovery in economic activity since reopening has been robust. J.P. Morgan noted that all the states analyzed (19) recorded double digit revenue declines in April, but in July experienced an average 63% increase in income tax collections year-over-year. The State of Ohio in its recent monthly financial report noted August tax receipts were robust and that “Nonauto sales tax, auto sales tax, and personal income tax exceeded estimates by percentages ranging from three percent to ten percent.”[4] Interestingly, it noted the dynamic nature of sales taxes: following the 2Q decline, the economic climate and pandemic realities have caused “shifts in consumption away from services and toward goods.”

Information that we track for Illinois’ local government sales, income and use tax collections distributed to local governments seem to support some of the conclusions arrived at by J.P Morgan and the State of Ohio, as well. Sales tax collection data is available up to and including sales made in June 2020 – declines began in March with 17% lower collections in that month versus the same month in 2019. Declines of 30% and 23% followed in April and May. The data for June provides a less clear comparison given an apparent reporting discrepancy but still indicates that taxes may have increased as much at 13% versus the prior period. For the rolling 12-month period as of June 2020 then, sales taxes were down around 3% with significant variability at the local level (note too that this data isn’t wholly comparable to the state as it includes variations due to local sales taxes enacted by municipalities, not just a state wide tax).

Income taxes were down 50% in April versus April 2019, virtually breakeven in May and June then more than doubled the 2019 period in July before recording a 29% increase in August – on a rolling 12-month basis this amounted to 2-3% increase as of August 2020 (compared to a 6-7% decline if the endpoint was April 2020). Finally and interestingly, use taxes[5] in Illinois appear to have benefitted from internet sales and did not report a year-over-year decline on a monthly basis over the last six months, with the rolling 12-month total up 20% as of June 2020. As the state of Illinois is more reliant on income taxes than sales taxes, these results so far appear generally favorable although likely caused liquidity pressure due to the significant swings in income tax collections. At the local level, distributions of sales taxes (rolling 12-month total of approximately $4.12 billion) far outweigh income tax (approximately $1.38 billion) or use tax (approximately $387 million) distributions.

****

Thus it seems that more volatile sources of operating revenue for many credits issuing general obligation bonds have performed better than anticipated, though impacts still appear to be broadly negative with the possibility of lingering cumulative impact depending on the trajectory of the pandemic.

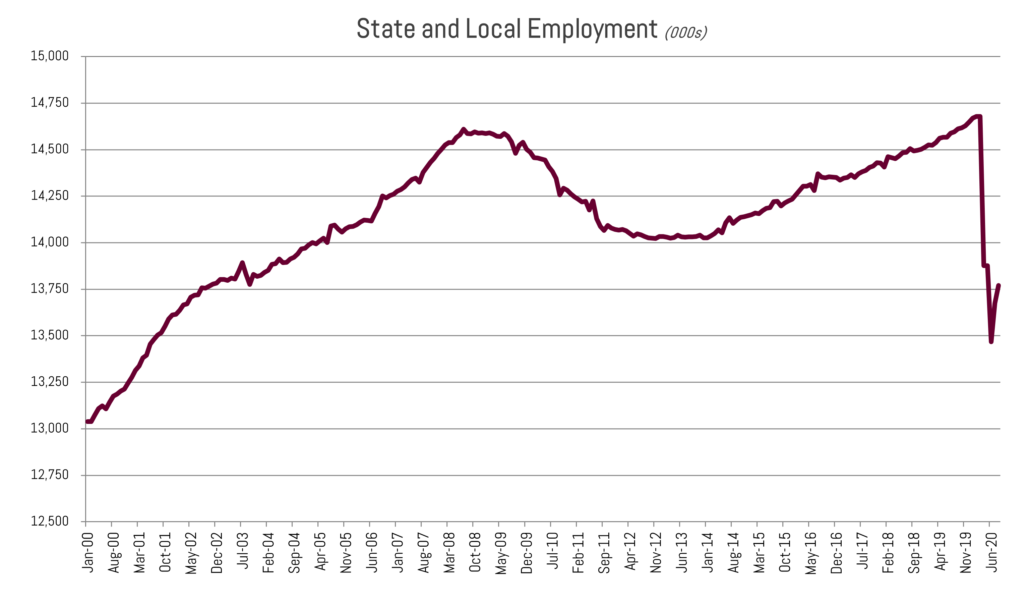

As of now, many issuers have reacted to the revenue uncertainty by reducing discretionary operating expenses (such as travel, certain fringe benefits, training, etc.) and postponing capital spending where possible. Some have frozen or even reduced headcount. The Bureau of Labor Statistics data indicated state government employment as of August 2020 compared to February 2020 is down 4% while local government employment is down 6% – nearly 1 million jobs in total. Although these percentages are actually below many private sectors of the economy over the same period, it is important to note that the percentage increase in total private employment from July 2008 to February 2020 was 12-13% whereas state and local government increased less than 0.5%, respectively over the same time period.

Source: U.S. Bureau of Labor Statistics

Source: U.S. Bureau of Labor Statistics

Although federal aid has certainly benefitted issuers in dealing with direct costs of the pandemic (in particular for sectors such as airports, mass transit and universities), most of the municipal sector has not seen much, if any, direct federal aid to counteract tax revenue losses (though there has been indirect support, such as increased unemployment benefit payments and the Paycheck Protection Program). Proposals for additional federal aid that in part specifically address such government revenue shortfalls have been mired in partisan disagreements about the size and scope of any stimulus plan with attempts at a compromise still ongoing.[6]

As we noted in our Market Review, the market’s perceived timetable for another round of stimulus was far too optimistic and additional aid to municipalities may not come until after the election. Although state and, in particular, local governments largely avoided assuming the receipt of such federal aid in their budgets, those that did—such as the state of Illinois[7] – are experiencing additional budgetary pressure.

These data points indicate that while revenue sources for many issuers of general obligation and essential service revenue bonds have been negatively impacted, they still performed better than initially anticipated over the last few months of the pandemic. It is important to recognize there is significant variation at the local level and we expect this to continue. Lastly, certain municipal sectors carry significant operational and credit risk even beyond the challenges to most general obligation and essential service bond issuers:

- Health care; in particular, nursing and retirement care

- Mass Transit and airport revenue; in particular, credits unsupported by tax revenue or supported by narrow sources of tax revenue (the Metropolitan Transportation Authority in New York City remains on negative outlook. S&P has downgraded several airport credits over the last month while maintaining a negative outlook on most)

- Narrowly focused, dedicated tax bonds (e.g., hotel/motel taxes, food & beverage or restaurant sales taxes)

- Higher education; in particular, credits with a more narrow revenue pledge limited to auxiliary revenues (housing & dining services, parking revenues or even student fees). As well as regional state universities and private universities without solid national brand recognition

These types of credits remain more exposed to either elevated costs or sudden declines in revenue (or both) as a result of the pandemic. It remains to be seen, for instance, the ultimate operational impact from the pandemic on universities. Many have invited students to return to campus while many others have discouraged or forbidden students to return for the fall semester. These decisions, of course, have affected systems’ revenues collections and there is no clear solution in sight. Given universities’ ability to shift many classes online, the negative impact is ameliorated somewhat, but this approach may fail in the end if students tire of it. However, even if students remain on campus, with outbreaks remaining a persistent issue, collection of auxiliary revenue and student fees could be negatively impacted – for instance universities in Utah announced fee waivers[8] coming into the 2020-2021 year.

There remains a possibility of a resurgence of COVID-19 in the fall to early winter similar to what many states experienced during late June and July. Additional longer-term pressure could arise depending on the efficacy of a vaccine in terms of not only initial immunity but the durability of immunity from COVID-19[9]. The less effective and durable a vaccine, the larger and more extended the negative impact on these highlighted sectors and indeed, the broader economy and municipal landscape.

Considering this, it appears downside risk remains in the municipal market and in particular, the most vulnerable sectors including health care, transportation, higher education and certain dedicated tax bonds. However, the general obligation and essential service revenue sectors of the market appear to be better positioned to weather this continued pandemic as they have done over the past several months. In particular, we continue to focus on issuers with broad tax or service bases that are better positioned to avoid social unrest and environmental stress (both of which compound the already daunting challenge of the pandemic) as well as areas less reliant on tourism and operating revenue streams less reliant on volatile types of taxes.

Brian Shea

Director of Municipal Credit

Matt Bernardi

Vice President, Investment Specialist

[1] https://www.cbpp.org/research/state-budget-and-tax/states-grappling-with-hit-to-tax-collections

[2] https://www.bostonfed.org/news-and-events/news/2020/07/cpp-covid-state-revenue-impacts-zhao.aspx

[3] JPMorgan Municipal Morning Intelligence, September 2nd, 2020

[4] https://archives.obm.ohio.gov/Files/Budget_and_Planning/Monthly_Financial_Report/2020-09_mfr.pdf

[5] According to the Illinois Department of Revenue, “Sales tax is a combination of ‘occupation’ taxes that are imposed on sellers’ receipts and ‘use’ taxes that are imposed on amounts paid by purchasers.” Refer to https://www2.illinois.gov/rev/research/taxinformation/sales/Pages/rot.aspx, https://www2.illinois.gov/rev/questionsandanswers/Pages/131.aspx, https://www.illinoispolicy.org/illinoisans-will-pay-higher-online-sales-tax-starting-in-2020/

[6] Refer to recent news articles, though this situation remains fluid:

https://about.bgov.com/news/what-to-know-in-washington-house-moderates-plan-stimulus-bill/

https://www.washingtonpost.com/us-policy/2020/09/22/congress-white-house-shutdown-stimulus/

[7] https://www.chicagobusiness.com/government/illinois-may-look-more-junk-pressure-rises-sp-says

[8] https://www.deseret.com/utah/2020/8/18/21374177/utah-public-universities-student-fees-fall-waiving

[9] Refer to https://www.cidrap.umn.edu/covid-19 and https://www.cidrap.umn.edu/covid-19/podcasts-webinars for commentary on the COVID-19 pandemic from a public health perspective