Tax Reform and Its Impact

December 2017

By Matthew P. Bernardi

Tax reform largely left the municipal bond market intact, though a bit squeezed, and it remains an attractive space for individual investors. We are satisfied with the outcome and are also grateful as American citizens and taxpayers that Congress largely left the market unhindered in its ability to fund the bulk (~75%) of our nation’s infrastructure.

Municipal bond investments serve two main purposes in any investor’s portfolio: principal preservation and a dependable stream of income exempt from federal income taxation. Another attractive feature that is often overlooked, is the direct impact investors have on local communities by providing attractive financing for essential public purpose projects.

After great efforts by local leaders and constituents during the reform debate, Congress heard this message: preserve tax-exemption because it plays a paramount role in financing our nation’s infrastructure and keeps costs low for taxpayers and community residents and businesses across the nation.

Impact on Market Dynamics

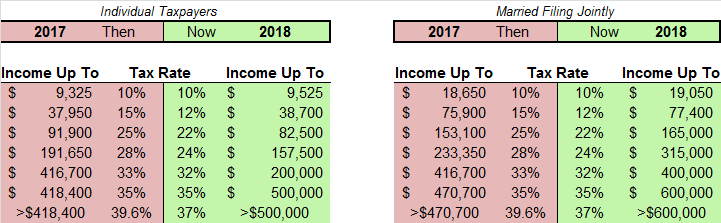

From a demand perspective, we believe tax rate changes will have a limited impact on individual investor interest. Below is a side by side graphic of changes to rates and income levels as a result of tax reform.

Source: Tax Cuts and Jobs Act

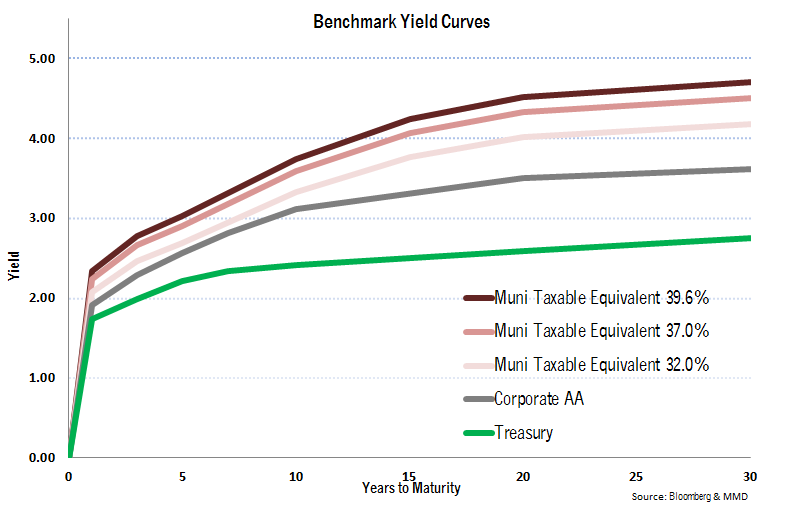

For top earners, lower top tax brackets will slightly reduce the attractiveness of tax-exempt securities. The tax cut is minor and we do not believe it will have a meaningful impact on demand from this investor group. Taxable equivalent yields barely budge when taking into account the cut from 39.6% to 37% – even all the way to 32% (see graph below). Additionally, the 3.8% Medicare tax on investment income does not affect municipal interest.

For top tax bracket individuals, non-taxable bond yields remain more attractive than high grade fixed income alternatives.

As of 12/29/2017

That said, many investors who previously fell into the 28% bracket may realign in 22-24% range. This investor group should consider our taxable strategies. Please discuss details with your Bernardi Investment Specialist.

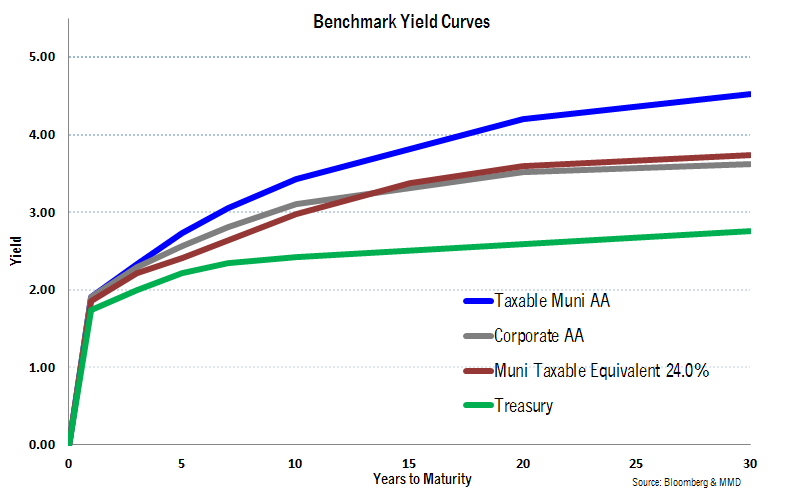

The graph below depicts the attractiveness of taxable municipal yields compared to taxable equivalent yields (TEYs) at the 24% tax bracket.

As of 12/29/2017

When designing portfolios, the balance between tax-exempt to taxable municipals depends on one’s projected tax rate, which we aim to project over the average maturity of the portfolio. In these cases, a dynamic approach to buying tax-exempt and taxable securities most likely provides the most attractive after-tax returns.

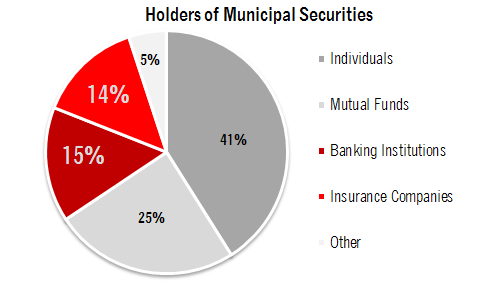

The muted effect on demand from these minor changes in individual tax rates may contrast sharply with the steep reduction in corporate tax rates, which are also permanent unlike the new individual tax rates. Demand for tax-exempt bonds likely will be significantly lower from institutional investors that are currently paying near or the top corporate tax rate. It also has the potential to make the Bank Qualified status of bonds an unnecessary qualification for issuers. The great unknown is whether the drop off in demand from this sector will push bond yields higher.

Banking and insurance companies own almost 30% of the market. With corporate tax rates falling from 35% to 21%, demand for municipals from these types of institutions will decrease unless yields adjust higher.

A positive of the tax reform law, from a supply perspective, is that Congress maintained the ability for issuers to finance certain projects through Public Activity Bonds (PABs). This will continue to allow hospitals, affordable housing projects, and airports to finance valuable infrastructure projects with tax-exempt bond issues.

The elimination an of issuer’s ability to advance refund debt is the most significant setback coming from the tax bill. Prohibiting issuers from executing economic re-financings is a flaw in the law. Well managed issuers should have the ability to take advantage of low yields and refinance debt when significant savings are available. Eliminating this option for issuers will have a meaningful impact on supply in 2018.

From a credit quality perspective, tax reform will hopefully drive economic growth and make America a more attractive place for corporations to locate and invest. Lower income taxes may also stimulate consumer spending, thereby providing a boost to sales tax revenue. These economic catalysts, should they occur, will certainly benefit fiscal balances and the underlying credit health of the average municipality.

*****

Municipals will continue to play a vital role in one’s asset allocation and an important role in building this country. That said, a dynamic approach may be needed when investing in the market based on the yield curve. Please reach out to your investment specialist with any questions you have about the impact tax reform has on your municipal portfolio.