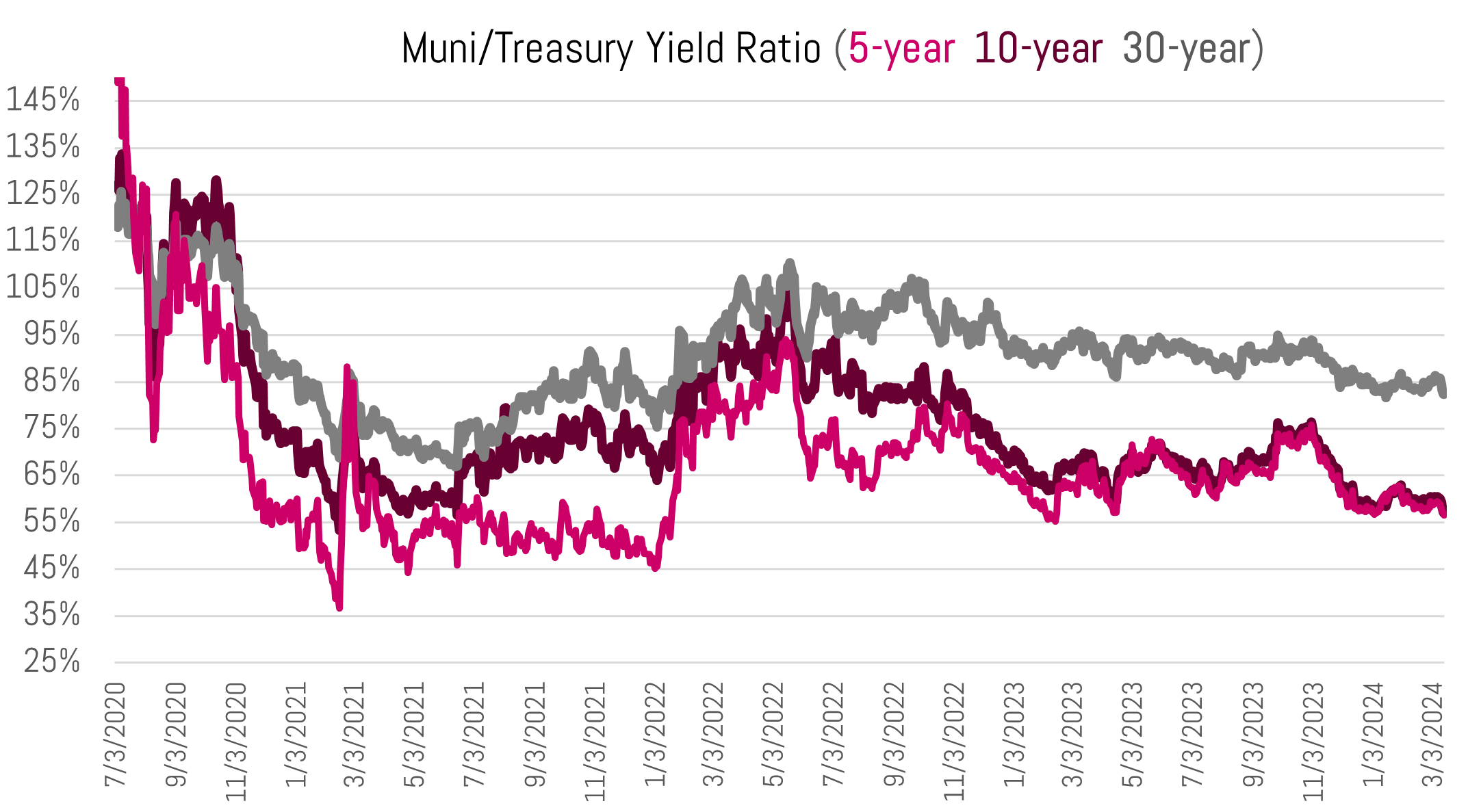

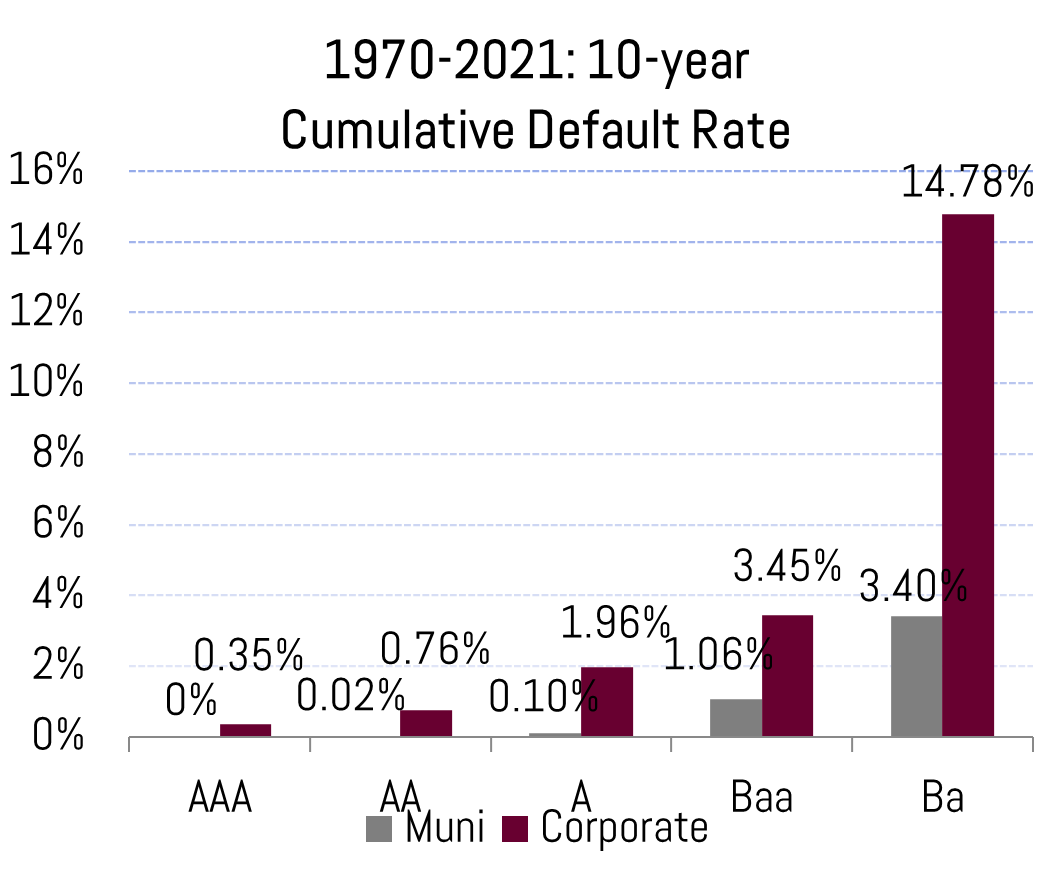

Municipal tax-exempt yields maintain fair overall valuations amidst a significant pick-up in supply throughout the year. The 10-year muni/treasury ratio is 69% vs. a 5-year average of 71%.[1] As of early September, total muni supply is up 38% year-over-year.[2] As we enter the final quarter, the pace of new supply should escalate further potentially pressuring ratios higher. Therefore, we think this fall could present opportunities to capture relative value in municipals should supply remain ample and the economy avoid a major slowdown. That said, investors remain awash in cash and any outsized move in municipal yields likely will be met with increased demand, bringing ratios back in check.

Source: SIFMA, September 2024

Greater supply is a welcome dynamic for a market which has essentially flatlined around $4 trillion total outstanding the past 15 years. This is during a timeframe where GDP has nearly doubled[3], money supply is up 250%[4], and treasury debt outstanding has moved from $8.8 trillion to over $27 trillion.[5] During this time, municipalities have generally not embarked on a debt-laden spending spree in effort to right size balance sheets post Great Financial Crisis. Furthermore, federal pandemic stimulus stuffed state coffers allowing some municipalities the ability to pay down debt. Entering 2024, rainy day fund balances are at record levels[6], pandemic aid is over, average pension funding is increasing, while our country has a pronounced infrastructure deficit…this means time is ripe for municipal issuance to pick up its pace for the foreseeable future.

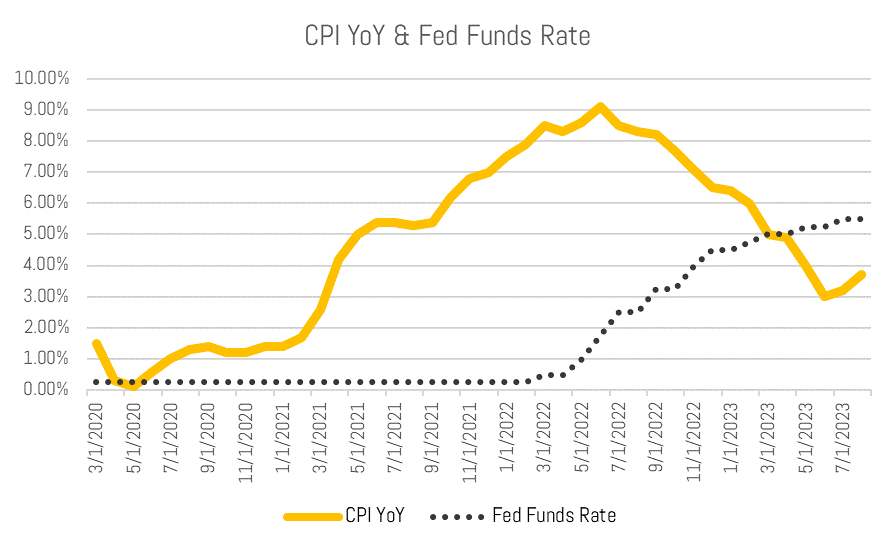

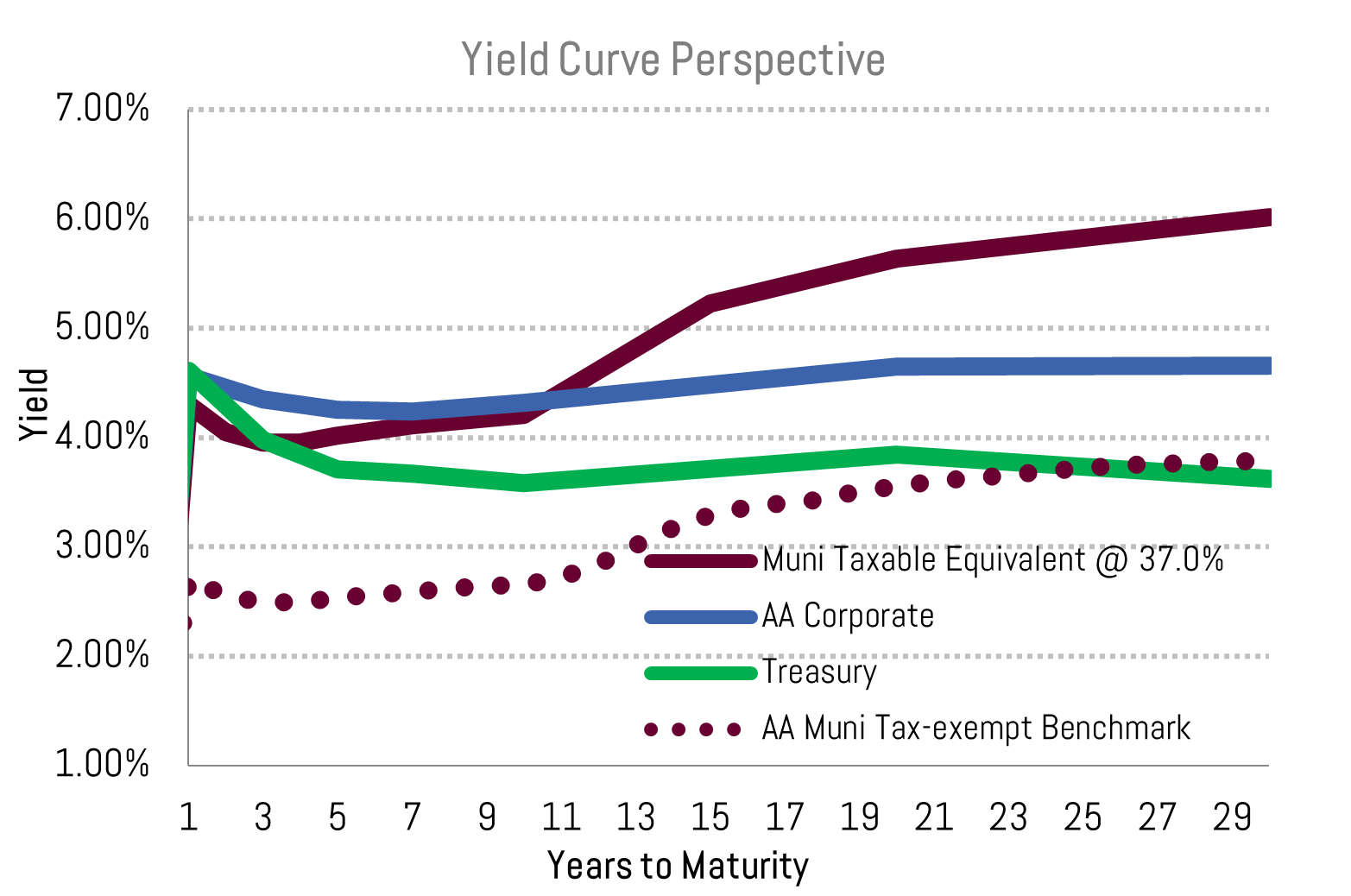

This should pressure ratios (the yield of a muni relative to treasury) higher, providing higher relative yields which favors income oriented investors. Currently the 10-year muni/treasury ratio is 69%, near its average since 2021. Prior to the financial crisis, from 2000 to 2007 it averaged 86%.[7]

This means the average 10-year municipal had a higher yield relative to the 10-year treasury from 2000-2007 than it has since 2021. A variety of inputs effect this ratio including the supply of bonds, the Federal tax code, the perceived credit health of municipalities, and the resulting demand dynamics for municipal bonds themselves.

At this point in time, given a favorable macro backdrop (as the Fed cuts rates /disinflation continues) and sturdy demand from investors, any outsized move higher in ratios has been largely kept in check by investor demand. Demand has been underpinned by investors seeking high nominal and after-tax-adjusted yield, which remain available even as the market prices in over 200 basis points (2%) of rate cuts through 2026.[8] Looking further out, as baby boomers continue to roll into their retirement years – and likely increase their fixed income allocation – this may provide an offsetting demand dynamic to digest higher levels of supply.

Furthermore, money market fund balances just recently reached an all-time high at $6.76 trillion.[9] Investor appetite therefore is plentiful, and should ratios become overly disconnected, we’d expect a quick recovery as investors seek value.

The chart above displays YTD municipal bond issuance in orange, which has significantly outpaced the prior 5-years of issuance. As we enter the last quarter of the year, historical seasonality trends point to an increasing pace of supply. Source: Bloomberg, September 2024.

Current Yield

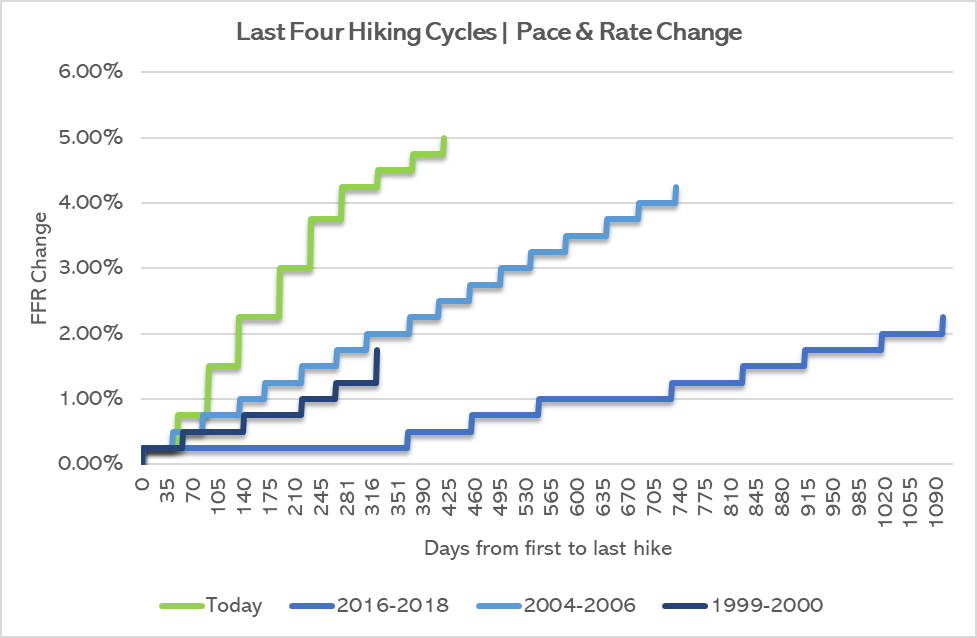

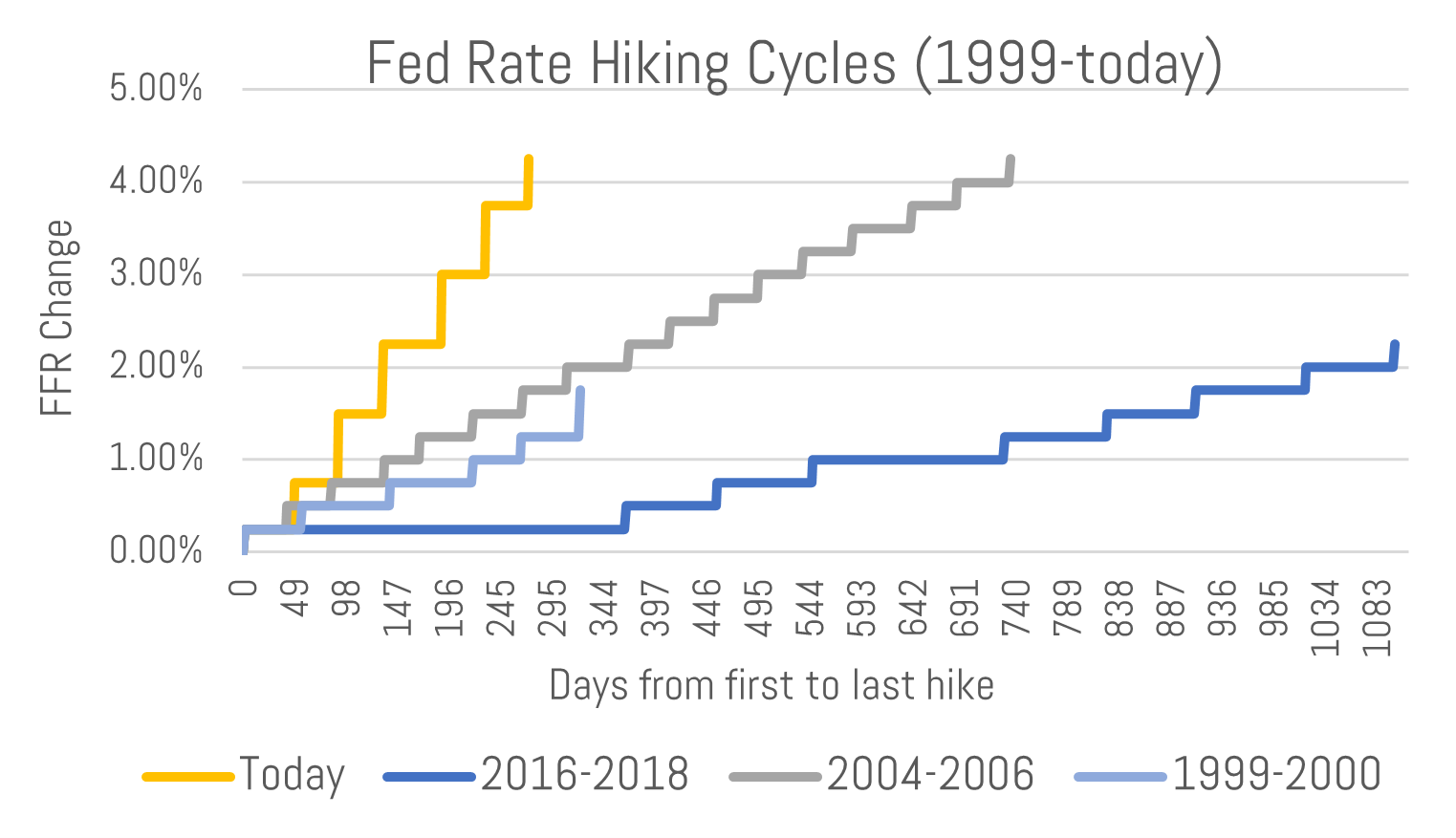

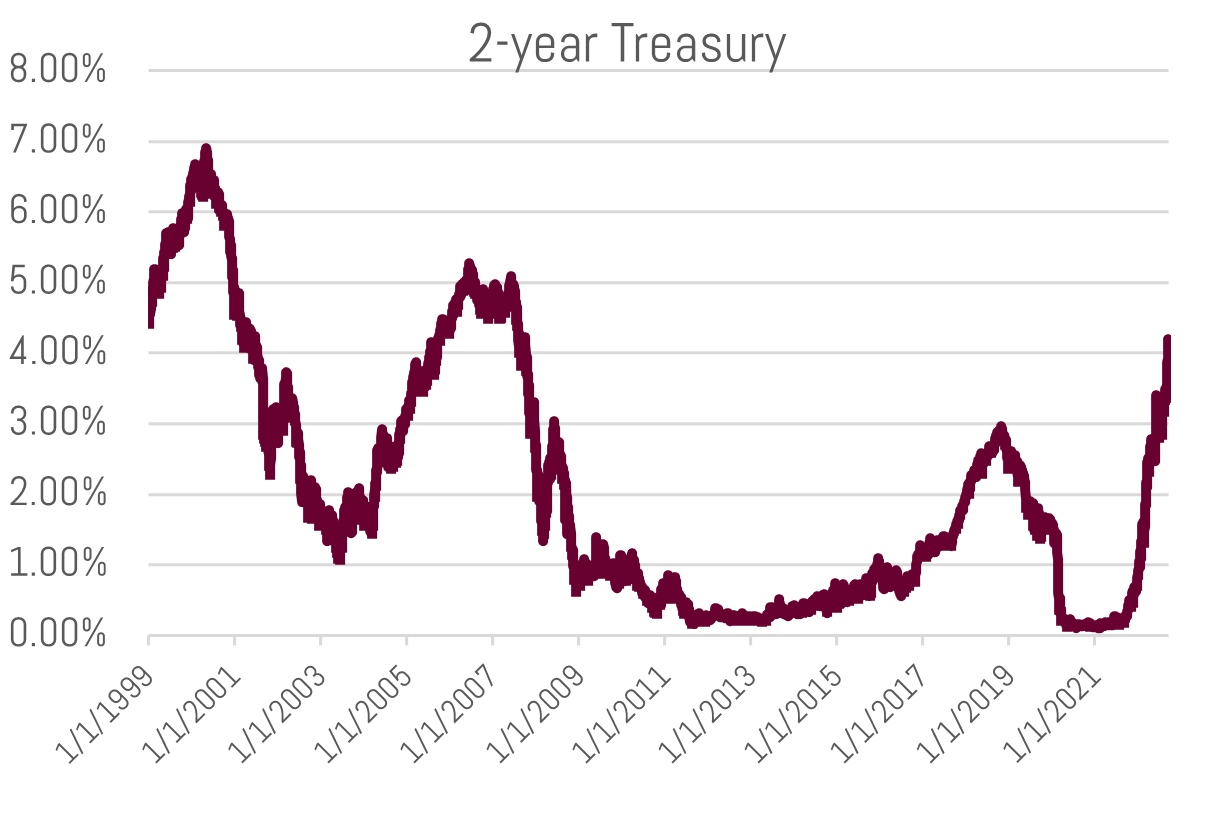

As the Fed cuts short term rates, we expect increased demand for intermediate-to-long duration bonds as cash moves off the sidelines away from deteriorating short term rates. The Fed currently is signaling an aim for a ~3% Fed Funds Rate (down from 5% today) to be reached over the next 2 years.[10]

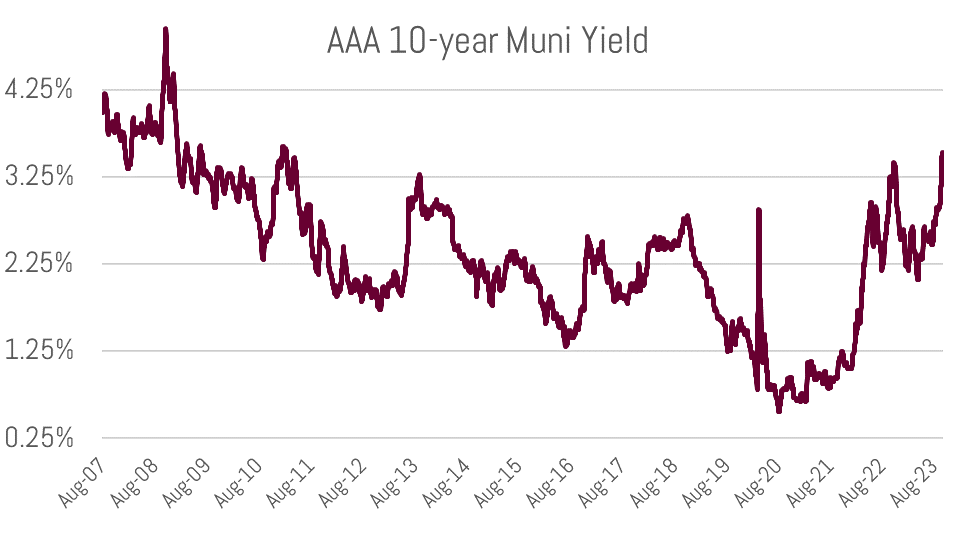

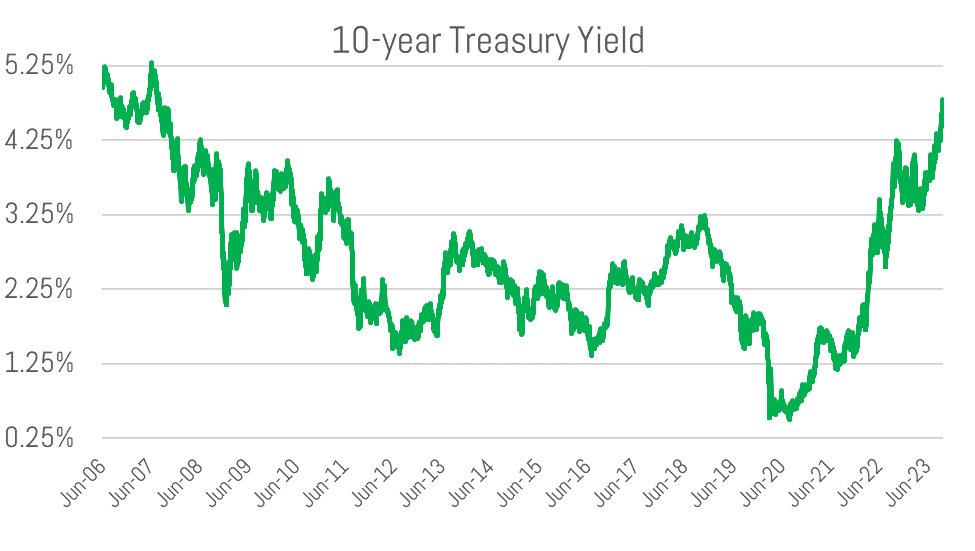

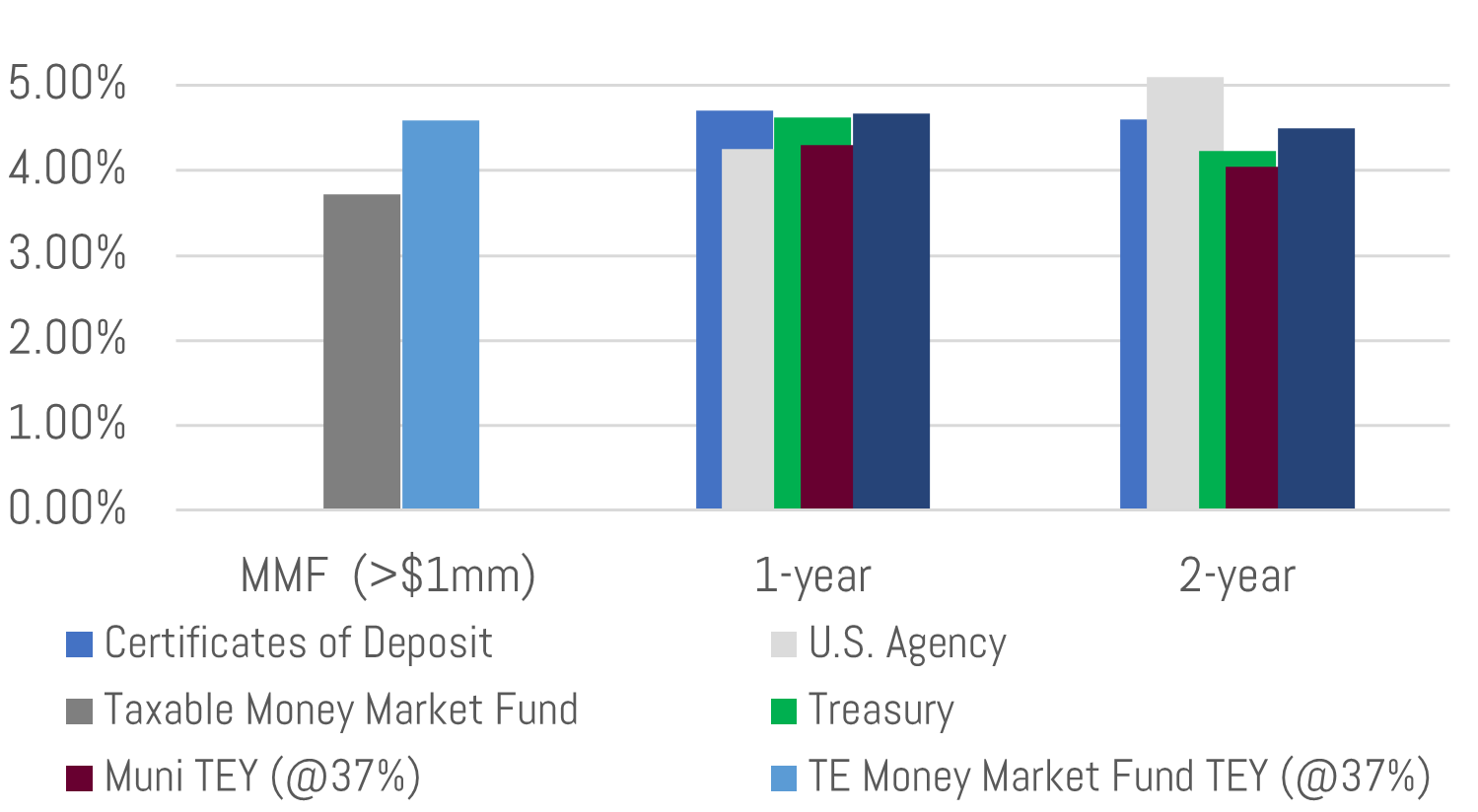

Regardless of what the future might hold for supply and demand dynamics, we believe today’s relative and outright yield levels remain attractive for municipal bond investors. Tax-exempt yields of 3.00%-4.00% for a portfolio with a max maturity under 15-years are still attainable. At the top income tax bracket, these yields are equivalent to taxable rates of 4.76%-6.34%. Today’s 10-year treasury yields under 3.80% while it has averaged 3.25% since the year 2000.[11]

Sincerely,

Matt Bernardi

Sr. Vice President

[1] Source: Bloomberg BVAL AAA Muni Yield % of Treasury 10-Year. To calculate the ratio you divide the municipal yield by the concurrent treasury maturity yield.

[2] https://finance.yahoo.com/news/muni-debt-sales-set-surge-180737417.html

[3] Source: https://fred.stlouisfed.org/series/GDP

[4] Source: https://fred.stlouisfed.org/series/M2SL

[5] Source: SIFMA

[6] “With an estimated aggregate $155.7 billion in savings at the end of fiscal 2024, states could run government operations on rainy day funds alone for a median of 48.1 days, equal to 13.2% of spending—a record high. The strength of state rainy day funds remained approximately 66% greater than in fiscal 2019, just before the pandemic-induced recession started in February 2020.” Source The Pew Charitable Trusts, Prioritize Reserves as Fiscal Flexibility Declines, September 19, 2024 https://www.pewtrusts.org/en/research-and-analysis/articles/2024/09/19/states-prioritize-reserves-as-fiscal-flexibility-declines?rsrv_hbar_data_picker=rdfd&rsrv_line_data_picker=tbd

[7] Source: Bloomberg BVAL AAA Muni Yield % of Treasury 10-Year (MUNSMT10 Index)

[8] Source: Fed Fund Futures, Bloomberg WIRP screen

[9] Source: https://cranedata.com/archives/all-articles/10499/

[10] Source: https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20240918.pdf

[11] Source: Bloomberg, September 26, 2024

Disclosures: All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. Past performance is no guarantee of future returns. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy will be profitable.