Market Update: As many market participants anticipated, on Wednesday, December 16th the Federal Reserve announced its first rate hike since 2006 increasing the fed funds rate to a range of 0.25% – 0.50%. Despite the news, municipal bond yields decreased during the fourth quarter with AAA 5-year, 10-year, and 20-year yields falling 2, 11, and 25 basis points, respectively. According to Bloomberg, the market is not projecting a rate hike during the Fed’s January meeting.

Market Update: As many market participants anticipated, on Wednesday, December 16th the Federal Reserve announced its first rate hike since 2006 increasing the fed funds rate to a range of 0.25% – 0.50%. Despite the news, municipal bond yields decreased during the fourth quarter with AAA 5-year, 10-year, and 20-year yields falling 2, 11, and 25 basis points, respectively. According to Bloomberg, the market is not projecting a rate hike during the Fed’s January meeting.

City of Worchester successfully issued $41.492 Million of Series 2015A General Obligation Municipal Purpose Bonds.

The Bonds are rated AA-minus by S&P, Aa3 by Moody’s, and AA-minus by Fitch.

The Bonds are being issued for the purpose of financing capital projects. The Series A Bonds are valid general obligations of the City of Worcester, Massachusetts and the principal of and interest on the Series A Bonds are payable from taxes which may be levied upon all property within the territorial limits of the City and taxable by it, subject to the limit imposed by Chapter 59, Section 21C of the General Laws. Chapter 59, Section 21C of the General Laws is frequently referred to as “Proposition 2 ½ “, and it imposes two separate limits on the annual tax levy of a city or town.

The primary limitation is that the tax levy cannot exceed 2 ½ percent of the full and fair cash value.

For cities and towns at or below the primary limit, a secondary limitation is imposed. This limitation stipulates that the tax levy cannot exceed the maximum levy limit from the prior fiscal year by more than 2 ½ percent subject to certain exceptions for new construction and revaluations.

Worchester maintains its tax levy below the primary limitation. The City currently has roughly $10 million in unused levy capacity and could raise its tax levy by that amount without the need to obtain a voter-approved override of the “Proposition 2 ½” limitation.

Below is a summary of the City’s tax levy history.

A more in-depth discussion of Massachusetts tax levies can be found on page A-30 to A-35 in the offical statement of the City’s Series 2015A Bonds.

Let’s slow down a bit before jumping to conclusions.

Here are several observations about the October 30th, Wall Street Journal article How Muni Bonds ‘Yield’ 4% in a 2% World.

Author Jason Zweig makes a valid point in asserting that yields cited in a typical custodian brokerage account statements may be misleading.

In our view, the typical custodian statement’s reporting of “current yield” – coupon divided by current market value – is inadequate and needs amplification. We have long held this view and, for that reason, over fifteen years ago began providing our portfolio managed clients with a proprietary quarterly portfolio report to complement their custodian’s statement. In concert, the custodial statement and Bernardi’s proprietary quarterly report provide an accurate, transparent, and thorough description of portfolio metrics. These include various yields an investor can reasonably expect to earn.

The author’s powerful assertions aside, keep in mind he is writing about CUSTODIAL statements. The article fails to discuss industry-wide regulations as to how bond offerings must be presented to investors upfront. Regulatory disclosure requirements, coupled with our own self-imposed internal procedures, offer robust protections to investors.

There are many required disclosures (MSRB Rule G-15). The rule exists to protect investors and requires financial industry participants to clearly disclose a bond’s yield to maturity and its yield to call/worst, if applicable. These yield calculations account for the inevitable premium amortization as a bond approaches maturity. Additionally, the executing broker-dealer is required to send the client a confirmation that details the yield to worst and the yield to maturity for premium bond trades. Regulations also require broker-dealers obtain fair and reasonable prices for the client given current market conditions (MSRB Rule G-30).

Therefore, an alert investor is well aware of a bond’s expected yield at the time he or she makes any financial commitment in a bond investment. The author’s not so subtle implication that broker-dealers and advisors are fooling investors by selling them illusory yields is disconnected from industry rule requirements.

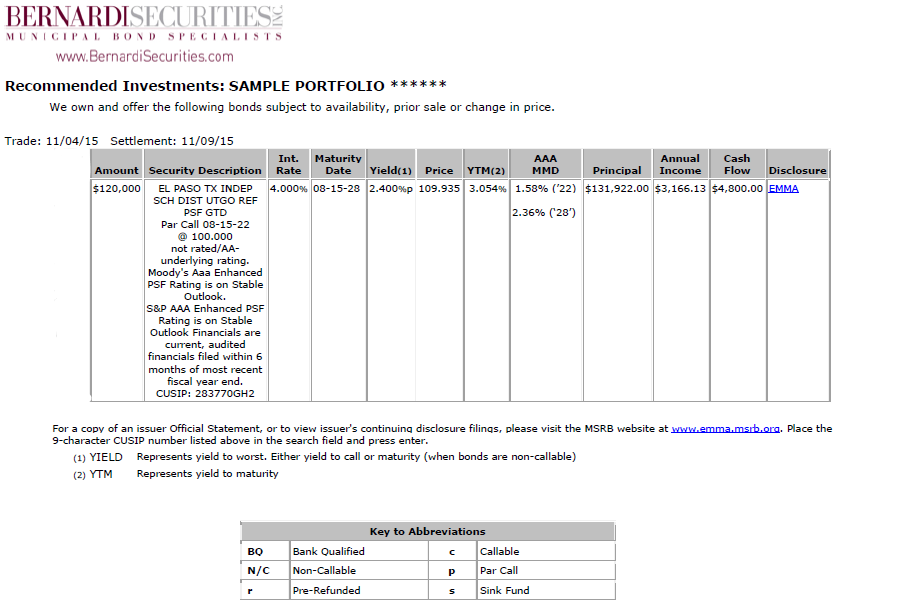

At Bernardi, we strive to provide complete transparency throughout our investment process. Below are two examples that help demonstrate our transparent and complete investment process and reporting. We use these documents in concert with one another in order provide investor clients with a thorough and robust description of portfolio metrics so they are comfortable with our process and how we report to them.

The graphic above is our portfolio management recommendation document. As you can see, the issue presented trades at a premium price. Yield to worst and yield to maturity metrics are featured as they represent the relevant yields. There is no mention of current yield in our presentation for reasons cited by Mr. Zweig. The “ANNUAL INCOME” figure cited for the premium issue represents actual income earned in the first year; the portion of cash flow representing amortized premium has been removed from the reported sum. This income figure is calculated by multiplying the yield to call/worst (2.40%) by the principal dollar investment ($131,922.00). Therefore, the client has all pertinent yield information to consider BEFORE he or she approves the recommendation. A trade confirmation is provided separately.

This last graphic detailed is a page from a Bernardi proprietary quarterly report. This report complements the custodial statement. Please note the sixth, tenth, and twelfth columns (highlighted). These show yield to maturity at cost, yield to call/worst at market, and yield to maturity at market.

Investing in bonds and reporting on bond holdings is not a simple endeavor. We purposefully provide a lot of detail offering our clients clear and robust reports.

The WSJ article is insightful, but, incomplete and misleading in certain respects.

We would love to discuss this topic with anyone interested. Thank you for your continued confidence.

Sincerely,

Ronald P. Bernardi

President/CEO

Market Update: Municipal bond yields decreased during the third quarter with AAA 5-year, 10-year, and 20-year yields falling 10, 25, and 21 basis points, respectively. In mid-September, the Federal Reserve reaffirmed its view to maintain the target range for the federal funds rate of 0.00% – 0.25%. As a result of the Fed announcement, the futures market is pricing in a fifty-percent chance that the first rate hike will not occur until March of next year.

Market Update: Municipal bond yields decreased during the third quarter with AAA 5-year, 10-year, and 20-year yields falling 10, 25, and 21 basis points, respectively. In mid-September, the Federal Reserve reaffirmed its view to maintain the target range for the federal funds rate of 0.00% – 0.25%. As a result of the Fed announcement, the futures market is pricing in a fifty-percent chance that the first rate hike will not occur until March of next year.

When is a bond manager a good fit for you?

What is the most economical way to pay for bond portfolio management services?

Does the manager adhere to a fiduciary or suitability standard?

What is the difference and does it matter to you?

Are you willing to pay ongoing fees for a fiduciary standard?

These are vexing questions for many investors and the appropriate answers depend on the differing needs and preferences of investors.

Today, regulators and industry participants are attempting to address disclosure, standards and transparency issues in a comprehensive manner. Balancing differing interests among investors makes this a difficult issue. How can investors be protected and offered choices without imposing anti-free market and overreaching rules on an already rules burdened financial services industry? Therein lies the rub.

At Bernardi, we regularly address these issues in discussions with our clients. Over the years, we have improved our portfolio management process and the way we offer and price our specialized management services. The objective of our Standards Committee is to design and implement processes that balance clients’ interests with ours.

A primary goal is to offer investors a choice while removing any confusion about our role and standards within the context of the available options. We offer investors two different bond portfolio management models because we believe a “one size fits all” approach to portfolio management does not benefit investors. We hold this view based on 30 plus years of specializing in the bond market, interacting with thousands of investors during this time and hearing from them which services best suit their needs.

First, let’s start with a few definitions.

A “fiduciary” standard requires the investment manager to put their client’s interest ahead of its own and fully reveal all compensation (direct and soft dollar payments) for investments it recommends. This is the gold standard in our industry and typically a more expensive option for investors.

A “suitability” standard requires a broker-dealer to recommend investments that are suitable (FINRA rule 2111). This standard requires the broker to deal fairly with investors and perform due diligence to ensure an investment is reasonably suitable for a specific client based on his or her needs, sophistication, risk tolerance and financial circumstances. The broker–dealer is also subject to the “Know Your Customer Rule” which requires it to know of and understand a client’s financial situation making it more likely investment recommendations will be suitable (FINRA rule 2090). Additionally, a broker-dealer will soon be subject to the pending MSRB “Best Execution” rule.

A SEC registered investment advisor (RIA) interacts with clients under the fiduciary standard, while a FINRA/SEC regulated broker-dealer is regulated by suitability, know–your-customer and many other rules protecting investors.

Department of Labor Proposal – Good Intentions, but Misses the Mark

The discussion surrounding these differing standards has been elevated recently because the Department of Labor (DOL) has proposed to expand the application of a best-interests standards (fiduciary) rule for broker-dealers working with retirement accounts. The proposed rule if adopted as currently written would treat anyone who provides investment advice or recommendations to an employee benefit plan, plan fiduciary, plan participant or beneficiary, individual retirement account or IRA owner as a Fiduciary under ERISA.

Presently, the proposed rule is in its comment phase following a multi-day public hearing in August.

There are differing opinions amongst industry participants and regulators as to which standard is appropriate and whether the standard should be universal. We support a harmonized multi-agency approach to developing a standard of care for broker-dealers in their interactions with investors based on these principles:

1. Clear disclosure of fees and mark-ups/mark-downs

2. Clear disclosure of any principal transaction activity

3. Clear disclosure of any material conflicts of interest

Our view of the proposed DOL’s rule is that it is confusing and overreaching. We view the fiduciary mandate rule for retirement advice problematic as currently written and here’s why:

- It favors an investment advisory (IA) business model over a commission–based model. This dynamic will reduce investor choice and increase ongoing costs for investors as many IRA accounts, currently at broker-dealers, would be forced to migrate to fee-based RIA accounts.

- The “Best Interest Exemption” portion of the rule restricts the assets available to investors: it allows for fixed income investing in U.S. Treasury bonds, corporate bonds and agency debt securities. It prohibits investors from transacting in taxable or tax-free municipal bonds under the terms of the exemption. Brokers cannot earn a commission related to a municipal bond transaction and the rule will result in many brokerage managed IRA accounts migrating to an RIA managed platform. The end result – the Rule will cause certain investors to pay ongoing RIA management fees if they want a laddered bond portfolio.

- The “Best Interest Exemption” requires two comparable quotes for a principal transaction. This requirement will delay the trading process. It is redundant as it ignores the pending “Best Execution” rule recently approved by industry regulator, FINRA and the already existing “Fair Pricing” rule.

The “Best Interest Contract Exemption” clause associated with the DOL proposal requires a broker-dealer to sign and commit to a legally binding fiduciary relationship with a client. Many broker-dealers will be reluctant, if not unwilling, to take on the additional regulatory and liability costs that flow from the fiduciary standard mandate.

The bottom line is this: certain investors will experience diminished choice or higher costs. Smaller retirement accounts, in particular, will experience this dynamic.

Unequivocally, there is a need to strengthen rules applicable to retirement accounts. However, neither FINRA nor the SEC, the two primary regulatory bodies that oversee broker-dealers, has signed onto the DOL proposal. Importantly, the rule needs to be uniform, not choice limiting and harmonized with other governmental agency rules. The DOL proposal, as currently written, fails on all three of these counts. Here is a link to DOL “Fact Sheet” of the proposed rule.

DOL rule proponents argue it is needed to reduce incentives that allow certain brokers to put clients into high–fee products. We agree with the DOL this potential for broker misbehavior needs tempering and it can be addressed in a simpler, less intrusive manner than the proposed rule.

The approach regulators took with the recently enacted Municipal Advisor (MA) Rule (MSRB Rule G-42) serves as an excellent template. The MA rule regulates how broker–dealers and municipal advisors interact with municipal bond issuers. The rule requires transparency and disclosure from broker-dealers and municipal advisors. It continues to evolve and municipal bond issuers are better protected because of the rule. Importantly, issuers decide whether they want to interact with an underwriter (broker-dealer) or prefer instead to pay a fee to have a municipal advisor, acting as a fiduciary, interact with the underwriter on its behalf. The rule does NOT mandate, but allows issuers a choice.

The DOL should attempt to duplicate the MA rule approach.

An Alternate Approach – Offer Investors Transparent Choices

More than twelve years ago we began offering two distinct bond portfolio management options. Each adheres to the three disclosure principles cited earlier. We discovered two things:

- Offering options eliminates investor confusion as to our role and how we are compensated

- Most clients appreciate having a choice as to how they engage us to manage their portfolios

Each platform offers our expert management, one under a fiduciary standard and the other under the suitability rule. A significant difference between the two options is how we are compensated: either through a fee-only or a one- time mark-up model.

Each option offers different choices to investors. Both offer a multi-step portfolio management approach ensuring a professional, fair and transparent process. Investors are made aware of costs and potential conflicts in both cases. Some investors cede discretion over their portfolio to us, others do not. Please reference www.bernardisecurities.com for more details regarding the two platforms.

“ ………the harder the conflict, the more glorious the triumph.”

These are the words of Thomas Paine and are applicable to the topic at hand. There is a great opportunity for our industry in acting properly and addressing the issues we are discussing.

We recognized the issues years ago and began offering these two platforms. Doing so has served our clients well. They like the transparency and choice that each offer.

We believe it is unreasonable to assume someone working under a suitability standard is untrustworthy, interested only in recommending a higher fee investment. I have heard many fiduciary standard proponents state and imply as much.

Similarly, we believe it is unreasonable to assume someone working under a fiduciary standard is automatically trustworthy and conflict free. There is a littered landscape of financial industry fiduciaries who lost and stole millions of dollars of their clients’ money.

The notion advanced by some that all fiduciaries are benevolent and anyone acting in another capacity is untrustworthy is nonsense. That kind of talk is more political than practical.

We are in favor of applying a uniform standard to broker-dealers requiring their interests are aligned with client interests. Candidly, we do not understand how a sustainable business can exist and grow using a different foundation. Trust and transparency are the foremost principles of a healthy client relationship. But, conflicts of interest are endemic to any successful enterprise and not inevitably harmful. There is nothing inherently wrong with conflicts and not all result in bad outcomes. It is how a conflict is managed that counts. Lastly, potential conflicts need to withstand a high burden of proof and it is our responsibility to show that, if a conflict exists, it actually serves our client rather than hurts them.

Here is a great example:

A client alerts us they need capital from their bond portfolio. One of our portfolio managers or traders solicit bids nationwide on portfolio holdings. Our bid solicitation process is a multi-step process designed to ensure fair, effective and transparent pricing. But if market uncertainty is elevated and national bidding interest is reduced on that particular day our client will receive below average bids. Oftentimes in these situations, Bernardi as a broker–dealer, steps in offering to buy a client’s portfolio positions at a meaningfully higher price than the best bid received from the nationwide bidding platform. We do not have the bonds placed with another client and instead use our capital to make a market and support our client who needs to sell.

Clearly, there is a potential conflict of interest here. But the fact is, the outcome for our client is better BECAUSE we interject ourselves into the process by using our capital and fulfilling an important marketplace role. The key to success for our client results from established company policies and a transparent internal process. Our process guides us to manage the conflict to help our client and it can withstand the burden of proof we are obligated to demonstrate if asked.

Conversely, here is an example currently confronting some advisors acting in a fiduciary capacity: many fee-only registered investment advisors are collecting fees from custodians for recommending certain mutual funds.

THERE IS NOTHING NECESSARILY WRONG WITH THIS CONFLICT PROVIDED THE ADVISOR HAS CLEARLY DISCOSED TO A CLIENT THE ARRANGEMENT, ITS PAYMENT TERMS AND BELIEVES THE FUND INVESTMENT IS SUITABLE FOR THE PORTFOLIO.

Just as in the first example, the advisor should understand the burden of proof needs to withstand scrutiny.

Investors Benefit from Aligned Interests and Choice

At Bernardi, we operate and design our policies and procedures with an overarching goal to align our interests with our clients’. This belief is fundamental to the way we operate our business. We do this by promoting high standards, educating our clients and serving them in a competent and professional manner. We have adjusted our business model many times over the years to better serve our clients and to conform to new regulations. We will continue to evolve and change as the world around us requires.

We stated earlier a “one size fits all approach” does not benefit investors. If a rule mandates such, of course, we will adapt. But in my nearly 35 year career I have learned this: investors demand different things and want choice.

Some want a fee only platform, while others prefer a one-time mark-up platform. Some want fiduciary management and are willing to pay an ongoing fee for the standard. Other investors are comfortable with managers adhering to suitability and know-your-customer standards and do not want to pay ongoing fees.

Regulatory rules should not dictate these decisions. Investors should be offered choices and allowed to decide for themselves.

Thank you for your continued confidence in our team.

Sincerely,

Ronald P. Bernardi

President and CEO

September 24, 2015

We thought you might find the attached white paper interesting. It is sponsored jointly by GFOA and IMCA and is authored by Justin Marlowe, professor at the University of Washington.

The paper describes the important role tax-exempt financing plays in funding infrastructure investment and how access to tax-exempt financing shapes state and local government investment in public purpose projects.

The paper addresses three critical issues facing municipal bond issuers:

- The sensitive nature of capital investment to fluctuating tax-exempt interest rates

- The lower cost of capital benefitting state and local governments due to tax exemption

- The effect on cost of capital if Congress repeals or sets an arbitrary cap on tax exemption

Here are several notable points detailed in the report:

- If federal tax exemption for municipal bonds did not exist, state and local governments would have paid more than $700 BILLION in added interest expense between 2000-2014.

- Approximately 90 percent of state and local capital spending is financed with debt. At the moment, alternative financing methods such as pay-as-you-go and public-private partnerships are effective for some types of capital projects, but are not a robust alternative to traditional municipal bonds.

- There is considerable elasticity in the supply of municipal bonds. Therefore, the presence of factors like high interest rates, threat to tax-exemption or capping the value of municipal bond interest at 28% does affect whether issues come to market and the interest rates paid.

- Calculations made by a number of groups overstate how much revenue the U.S. Treasury foregoes each year as result of the municipal exemption. In fact, Professors Poterba and Verdugo (2009) estimate the cost of the exemption is $14 billion each year. Their calculation is FIFTY PERCENT lower than recent calculations put forth by critics of municipal bond tax exemption.

We have written and spoken extensively on this topic over the last several years. Below are links to several of our publications on the topic:

White Paper: Tax-Exempt Municipal Bonds

Market Commentary: A Century of Tax-Exempt Municipal Bonds: The Good, the Bad and the Ugly

It is important that proponents of tax-exemption remain vigilant and informed to the ongoing threat. It is important that proponents continue to educate Congress, congressional staff and administration officials as to the important role tax-exempt bonds play in our communities.

Tax-exempt bonds are an established, time tested means for financing public purpose infrastructure projects for communities across our nation. Radical changes to the current market structure will result in higher financing costs for all, less infrastructure investment and a reduction in local control over the financing of community projects.

Please feel free to contact me if you have any questions or wish to further discuss this topic.

Sincerely,

Ronald P. Bernardi

President and CEO

August 27, 2015

Market Update: Municipal bond yields increased during the second quarter with AAA 5 year, 10 year, and 20 year yields rising 14, 32, and 34 basis points, respectively. Positive economic data, a surge in supply and anticipation of a rate increase by the Federal Reserve helped drive rates higher across the curve.

“If it looks like a duck, swims like a duck, and quacks like a duck, then it probably is a duck.”

This straightforward method of reasoning can often help one gain a better understanding of the intricate – yet ubiquitous – financial products of today. When applying the reasoning above, in the context of liquidity, it is discovered that a municipal bond mutual fund or ETF is surely not a bond (duck). The underlying assets are bonds, but the trading vehicle is far from a bond. The sometimes perceived “enhanced” liquidity ascribed to bond mutual funds compared to individual bonds, often has caused investors to experience greater loss in turbulent markets. Today’s market experts, from Howard Marks to Carl Icahn, have all recently warned about this paradigm and the dangers of illiquid mutual investment vehicles. In our experience, a separate account portfolio – where individual bonds are directly owned – is an advantageous bond portfolio structure in both stable and volatile times.

This straightforward method of reasoning can often help one gain a better understanding of the intricate – yet ubiquitous – financial products of today. When applying the reasoning above, in the context of liquidity, it is discovered that a municipal bond mutual fund or ETF is surely not a bond (duck). The underlying assets are bonds, but the trading vehicle is far from a bond. The sometimes perceived “enhanced” liquidity ascribed to bond mutual funds compared to individual bonds, often has caused investors to experience greater loss in turbulent markets. Today’s market experts, from Howard Marks to Carl Icahn, have all recently warned about this paradigm and the dangers of illiquid mutual investment vehicles. In our experience, a separate account portfolio – where individual bonds are directly owned – is an advantageous bond portfolio structure in both stable and volatile times.

The “mutualization” of the financial securities market in a little over a decade has been enormous. Total net assets in ETFs have grown from $119 billion in 2003 to over $1.4 Trillion today.[1] These funds essentially are the market. The growth of ETFs and mutual funds has many benefits for investors. Mutual investment vehicles enable scale, often decreasing costs and facilitating access to unique assets and strategies. For bond mutual-funds, “stock-like” liquidity is also a marketed benefit. However, there is an inherent mismatch between the daily liquidity of the vehicle and trading activity of the underlying assets (the duck has a tail fin). Bill Gross referred to this as a “liquidity illusion”[2] in his most recent market commentary. Liquidity exists in stable markets due to a balance of buyers and sellers. However, ETF liquidity is challenged (as displayed in 2008, 2009, and 2013) in times of market volatility. To put it more simply, mutual investors sell at fast-paced equity speeds when the off-ramps are more gradual-paced bond speeds. In this environment price has to give way for liquidity.

The “mutualization” of the financial securities market in a little over a decade has been enormous. Total net assets in ETFs have grown from $119 billion in 2003 to over $1.4 Trillion today.[1] These funds essentially are the market. The growth of ETFs and mutual funds has many benefits for investors. Mutual investment vehicles enable scale, often decreasing costs and facilitating access to unique assets and strategies. For bond mutual-funds, “stock-like” liquidity is also a marketed benefit. However, there is an inherent mismatch between the daily liquidity of the vehicle and trading activity of the underlying assets (the duck has a tail fin). Bill Gross referred to this as a “liquidity illusion”[2] in his most recent market commentary. Liquidity exists in stable markets due to a balance of buyers and sellers. However, ETF liquidity is challenged (as displayed in 2008, 2009, and 2013) in times of market volatility. To put it more simply, mutual investors sell at fast-paced equity speeds when the off-ramps are more gradual-paced bond speeds. In this environment price has to give way for liquidity.

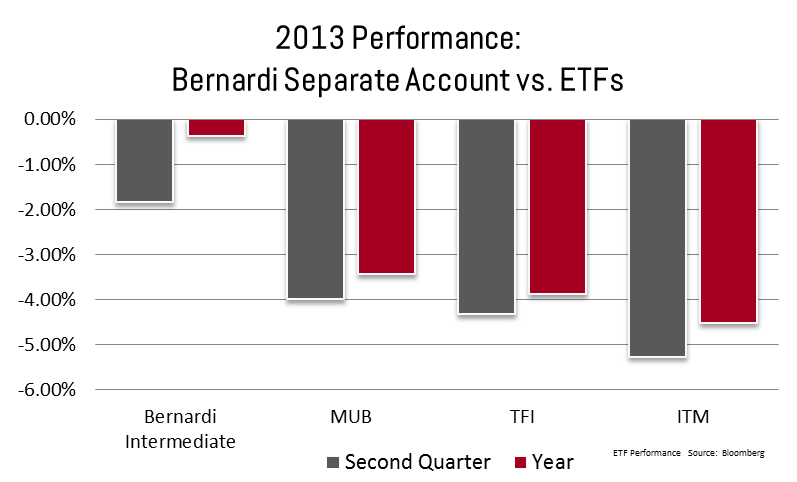

In times of market stress, our separate accounts outperformed major ETFs, as the ETFs demonstrated the shortcomings of their structure. For example, during the “taper tantrum” in June 2013, the Net Asset Value (NAV) discount on the MUB (the largest ETF that tracks the municipal market) was as large as 2.85%.

In 2013 our intermediate separate account portfolios were better able to weather the storm and outperformed during that quarter and over the course of the year (see chart).

Since 2013, ETFs and mutual funds have grown significantly and represent a larger share of the market. This growth has occurred as the underlying liquidity of bonds has dropped as banks have been forced to reduce their proprietary trading and overall market making activities. In response to concerns about the liquidity of the mutual funds in a bear market, fund managers have established a number of safeguards to protect against potential illiquid markets. These include larger cash balances, the use of derivatives, or even lines-of-credit to help fund investor withdrawals. In our opinion, such safeguards reduce return and increase costs.

Mutual funds certainly can serve an important purpose in any investor’s portfolio, for both return and diversification purposes. But ducks can naturally only fly so fast – it is not possible to repackage an asset and enhance the liquidity without taking on structural risk or additional costs. In our opinion, most of the vehicles currently available are a blend of both. On the other hand, a separate account portfolio, composed of laddered, individual bonds, only needs to remain as liquid as your individual circumstances demand and is not based on other’s liquidity droughts. At Bernardi Securities, we do not strive to scale our portfolio management process to a one-size-fits-all, mutually-owned product. In effect, the separate account allows for greater control and ability to customize.

I hope this information is helpful and if you have any comments or questions, please do not hesitate to contact your Investment Specialist or Portfolio Manager.

Sincerely,

Matthew P. Bernardi

Investment Specialist

Outside recent articles focused on this popular topic of bond liquidity:

http://www.bloomberg.com/news/articles/2015-06-21/the-3-words-that-count-in-bonds-liquidity-liquidity-liquidity

http://www.bloomberg.com/news/articles/2015-07-27/oaktree-s-howard-marks-echoes-icahn-warning-on-junk-debt-etfs

https://www.janus.com/bill-gross-investment-outlook

Related articles:

Outperforming the Madness of Municipal Bond Fund Herds

Premium Municipal Bonds: Benefits in a Rising Rate Environment